Anti-Money Laundering (AML) regulations are reshaping how Bitcoin payment gateways operate. These rules aim to combat financial crimes by enforcing strict compliance requirements, such as customer verification, transaction monitoring, and reporting obligations. Bitcoin payment gateways - acting as intermediaries between cryptocurrencies and traditional finance - must navigate complex international frameworks like the FATF Travel Rule, U.S. Bank Secrecy Act, and EU AML standards. Non-compliance can result in severe penalties, including multi-million dollar fines and reputational damage.

Key takeaways:

- FATF Travel Rule: Requires sender/receiver details for transactions above $3,000 (U.S.) or risk-based thresholds (EU).

- U.S. Regulations: Mandate registration with FinCEN, reporting suspicious activities, and maintaining transaction records for five years.

- EU Framework: Focuses on risk-based assessments, beneficial ownership verification, and reporting all suspicious transactions.

- Challenges: High compliance costs, fragmented regulations, and risks from unhosted wallets or mixing services.

- Solutions: Real-time monitoring, blockchain analytics, and automated compliance tools like Flash's non-custodial wallet model.

Bitcoin payment gateways must adopt advanced compliance strategies to meet these regulations while maintaining operational efficiency.

Crypto Compliance Crash Course: Master MiCAR & AML

How AML Directives Affect Bitcoin Payment Gateways

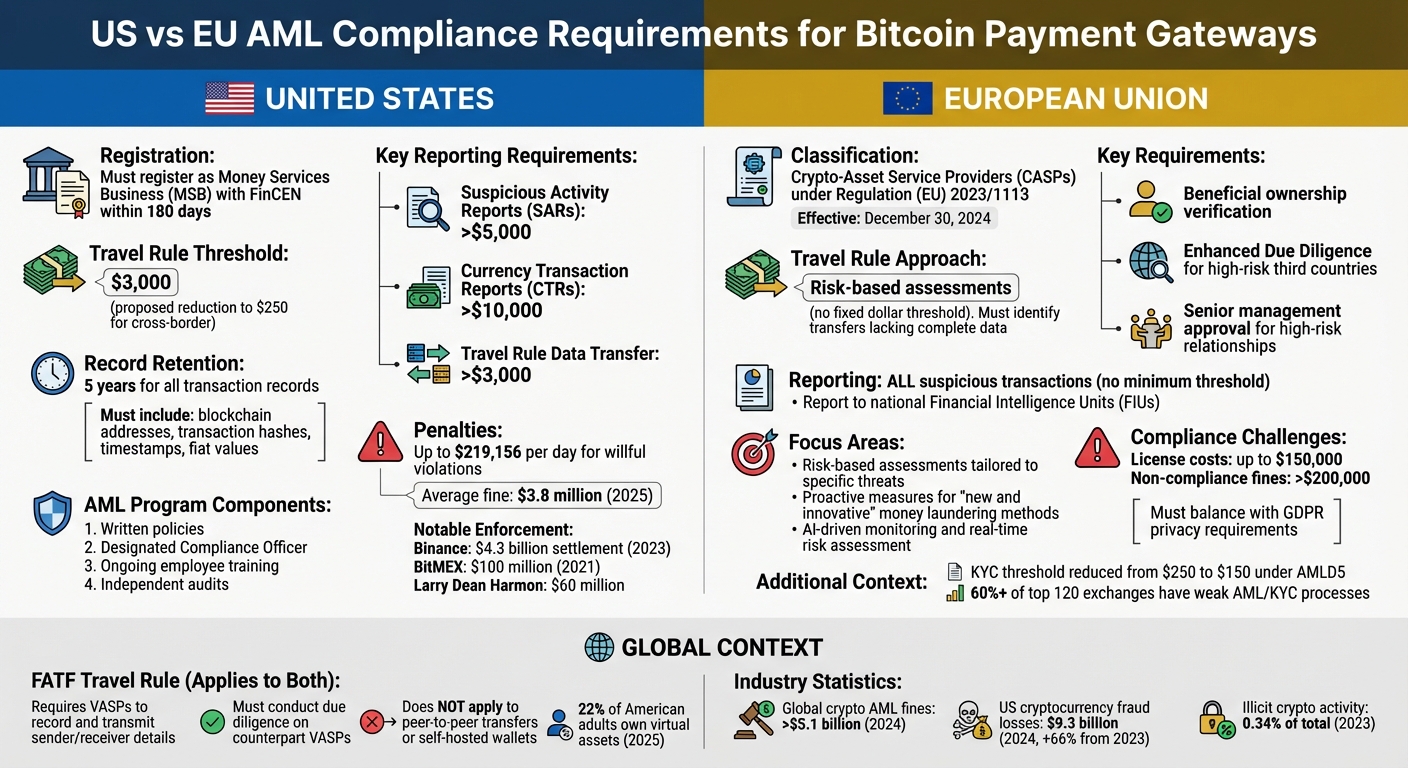

AML Compliance Requirements Comparison: US vs EU Bitcoin Payment Gateways

Navigating compliance is a core challenge for Bitcoin payment gateways. These platforms must operate within a maze of international and national anti-money laundering (AML) regulations, shaping how they process transactions and making compliance a critical part of their operations.

The impact of these regulations depends heavily on the jurisdiction. In the United States, Bitcoin payment gateways are required to register as Money Services Businesses (MSBs) with FinCEN within 180 days of starting operations. In the European Union, these platforms fall under the classification of Crypto-Asset Service Providers (CASPs), obligating them to monitor and manage transfers that lack complete sender or receiver details. Globally, the Financial Action Task Force (FATF) enforces its "Travel Rule", which requires Virtual Asset Service Providers (VASPs) to collect and transmit specific data about the originator and beneficiary with every transaction.

The financial penalties for non-compliance can be severe. For instance, in November 2023, Binance reached a $4.3 billion settlement with the U.S. Department of Justice, and CEO Changpeng Zhao was personally fined $50 million. Similarly, Larry Dean Harmon faced a $60 million fine from FinCEN for violating the Bank Secrecy Act, and BitMEX paid $100 million in 2021 for operating without adequate AML measures.

FATF Travel Rule Requirements for VASPs

The FATF Travel Rule (Recommendation 16) mandates that Bitcoin payment gateways classified as VASPs record and transmit key sender and receiver details for each transaction. Much like how wire transfer information is handled in traditional banking, this data must "travel" with the transaction. The goal is to enhance transparency, allowing authorities to track illicit funds and spot suspicious activity.

Compliance with the Travel Rule is no small task. Gateways must conduct thorough due diligence on their counterpart VASPs to avoid facilitating transactions with high-risk or non-compliant entities. This involves verifying that recipient institutions hold proper licenses, have effective AML programs in place, and are not located in jurisdictions flagged for money laundering risks. To meet these requirements, platforms often rely on specialized protocols for secure data exchange and deploy automated systems to monitor compliance in real time.

However, the Travel Rule does not apply to peer-to-peer transfers or transactions using self-hosted wallets, leaving a regulatory gap. With approximately 22% of American adults owning virtual assets by 2025, up from 20% in 2024, the importance of addressing these gaps is growing.

US AML Regulations: Bank Secrecy Act and FinCEN Guidelines

In the U.S., Bitcoin payment gateways registered as MSBs face stringent AML requirements. The current FinCEN threshold for triggering the Travel Rule is $3,000, though a proposal to lower this to $250 for cross-border transactions is under consideration. If enacted, this change would significantly increase the number of transactions requiring full data collection.

Gateways must also meet additional reporting obligations. Suspicious Activity Reports (SARs) are required for transactions exceeding $5,000 that raise red flags, while Currency Transaction Reports (CTRs) must be filed for cash transactions over $10,000. Transaction records - including blockchain addresses, transaction hashes, timestamps, and fiat values - must be retained for five years. Non-compliance can lead to steep penalties, with FinCEN authorized to impose civil penalties of up to $219,156 per day for willful violations.

| Requirement | Threshold | Reporting Form |

|---|---|---|

| Suspicious Activity | >$5,000 | SAR |

| Cash Transactions | >$10,000 | CTR |

| Travel Rule | >$3,000 | Data Transfer |

Gateways are also required to establish a formal AML program with four key components: written policies, a designated Compliance Officer, ongoing employee training, and independent audits. Customer Due Diligence (CDD) is a must for all clients, with Enhanced Due Diligence (EDD) applied to high-risk customers or transactions. By 2025, the average fine for AML violations in the crypto industry reached $3.8 million, with global fines exceeding $5.1 billion in 2024.

EU AML Framework and New Compliance Standards

In the EU, Bitcoin payment gateways must comply with Regulation (EU) 2023/1113, which took effect on December 30, 2024. This regulation requires platforms to establish procedures for identifying transfers that lack complete Travel Rule data. Unlike the U.S. system, which uses dollar thresholds, the EU approach focuses on risk-based assessments tailored to specific threats.

One major requirement is verifying beneficial ownership. This means identifying the individuals who ultimately control a legal entity, even when those individuals are obscured by complex corporate structures. This process becomes especially challenging when dealing with international clients using multi-layered holding companies. Enhanced Due Diligence is mandatory for dealings with entities from "high-risk third countries" identified by the European Commission, and senior management must approve such high-risk relationships.

All suspicious transactions, regardless of amount, must be reported to national Financial Intelligence Units (FIUs). This marks a departure from the U.S. threshold-based system and necessitates robust monitoring systems. The EU framework also encourages proactive measures to address "new and innovative" money laundering methods enabled by advancing technology. This pushes gateways toward adopting AI-driven monitoring tools and real-time risk assessment systems.

"The Travel Rule has seen significant divides in how different jurisdictions deal with its implementation and enforcement. Compliance is inconsistent, technology systems are often disconnected, and there's still some uncertainty about which specific benefits this rule brings to the table." - Kat Cloud, Head of Government Relations, Sumsub

Compliance Challenges for Bitcoin Payment Gateways

Bitcoin payment gateways face a maze of regulatory challenges, particularly when it comes to Anti-Money Laundering (AML) directives like AMLD5. These directives classify fiat-to-crypto services and custodian wallet providers as "obliged entities", requiring them to allocate substantial resources to technology, staffing, and legal compliance efforts.

The financial burden of compliance varies widely depending on the jurisdiction. For example, obtaining licenses in some regions can cost as much as $150,000, while fines for non-compliance might exceed $200,000. These steep costs have even prompted some platforms to relocate their operations. A notable case is the crypto derivatives exchange Deribit, which moved from the Netherlands to Panama in January 2020 to sidestep the high costs and slow processing times tied to Dutch AML and Countering the Financing of Terrorism (CFT) requirements.

Adding to the complexity, fragmented regulations force gateways to navigate a patchwork of jurisdiction-specific rules. Elsa Madrolle, International General Manager at CoolBitX, highlighted this challenge:

"The complexity of accessing Europe for any industry is exacerbated by the lack of a common regulatory regime. EU directives and regulations often have enough room for interpretation for national governments to apply their own political agenda".

Gateways also face the tricky task of balancing AML compliance with the General Data Protection Regulation (GDPR), which imposes strict privacy safeguards when handling identifiable user data.

Customer Due Diligence and Identity Verification

One of the biggest compliance hurdles for Bitcoin payment gateways is implementing robust customer due diligence procedures. This includes using eIDAS-compliant technology to support transparent Know-Your-Customer (KYC) processes. These systems go beyond basic identity checks, requiring verification of beneficial ownership in complex corporate structures.

Despite these efforts, many cryptocurrency exchanges still fall short. A study revealed that over 60% of the top 120 exchanges have weak or "porous" AML/KYC processes. Under AMLD5, the threshold for identifying users of electronic money and prepaid instruments was reduced from $250 to $150, making compliance even more demanding.

For high-risk customers, Enhanced Due Diligence (EDD) adds another layer of complexity. This involves additional scrutiny and continuous monitoring, which can strain compliance teams and significantly increase operational costs.

Transaction Monitoring and Reporting Requirements

Monitoring transactions in real time presents both technical and operational challenges. Traditional AML methods, which rely on trusted intermediaries, are less effective in the decentralized world of public blockchains. Bitcoin payment gateways, often serving as "off-ramps" to traditional banking systems, must rely on public transaction histories to trace the origins of cryptoassets.

To address this, many platforms are adopting automated scoring systems that evaluate the likelihood of illicit activity for specific cryptoasset units. A BIS Bulletin explains:

"An AML compliance score based on the likelihood that a particular cryptoasset unit or balance is linked with illicit activity may be referenced at points of contact with the banking system ('off-ramps')".

In addition to monitoring, gateways must meet demanding reporting requirements. This includes building infrastructure for Suspicious Activity Reporting (SAR) mechanisms, which securely share user data with authorities while maintaining strict data privacy. However, unhosted wallets and mixing services remain significant blind spots.

Risks from Unhosted Wallets and Mixing Services

Unhosted wallets and mixing services pose some of the biggest compliance challenges. Mixers, which blend cryptocurrencies to obscure the connection between sender and recipient, make it difficult to trace the origin of funds. As the Financial Action Task Force pointed out in 2024, such privacy-enhancing technologies are especially appealing to criminals because they are "hard to trace".

Unhosted wallets allow users to transact without involving a Virtual Asset Service Provider, leaving a large portion of the virtual currency ecosystem outside traditional AML monitoring. The European Parliament and Council acknowledged this limitation:

"The inclusion of providers engaged in exchange services... will not entirely address the issue of anonymity... as a large part of the virtual currency environment will remain anonymous because users can also transact without such providers".

Criminals exploit these gaps using advanced layering techniques, such as transferring assets across multiple addresses or even different blockchains through cross-chain swaps. These tactics make it nearly impossible for compliance teams to reconstruct complete transaction histories. A notable example occurred in April 2022, when U.S. and German authorities dismantled the Hydra darknet marketplace after analyzing Bitcoin flows to identify illicit wallet addresses.

To counter these risks, Bitcoin gateways must adopt more advanced screening measures at transaction points. Transactions originating from unhosted wallets or flagged high-risk services should trigger Enhanced Due Diligence. Automated tools can flag wallet addresses listed on sanctions databases, such as the U.S. OFAC Specially Designated Nationals (SDN) list, while blockchain analytics tools help trace illicit flows.

Some platforms are now integrating specialized tools to simplify these compliance tasks, aiming to bridge the gap between regulatory demands and operational efficiency.

sbb-itb-f81ab9b

How Flash Supports AML Compliance for Bitcoin Payments

Flash's Wallet-to-Wallet Model and AML Compliance

Flash operates on a non-custodial framework, which means it avoids the risks tied to intermediary fund handling. Payments flow directly between the customer and the merchant, thanks to Flash's wallet-to-wallet model. Importantly, the platform never takes custody of funds - merchants retain control throughout the transaction process. This setup eliminates the "honey pot" vulnerability often associated with traditional custodial gateways, which can attract money launderers.

By staying out of the transaction chain, Flash aligns with the risk-based approach outlined in the EU AML Directive 2015/849. This directive emphasizes maintaining financial integrity while fostering a regulatory landscape that allows businesses to operate without excessive burdens. It also highlights the importance of balancing privacy and data protection with anti-money laundering efforts. Flash's design minimizes sensitive data retention, streamlining AML record-keeping for merchants. On top of this secure foundation, the platform provides merchants with advanced tools for monitoring and compliance.

Flash Tools for KYC and Real-Time Monitoring

Flash's secure architecture supports effective Know Your Customer (KYC) processes and real-time transaction monitoring. The platform offers a dashboard with real-time analytics and reporting tools essential for compliance documentation. These analytics help businesses track transaction patterns and maintain the necessary records for Suspicious Activity Reporting (SAR).

Merchants connect their own Bitcoin Lightning wallets directly to the platform during setup. This approach ensures they maintain full custody of their funds while gaining access to Flash's monitoring tools. With this direct connection, businesses get complete visibility into their transactions, enabling automated risk scoring and early detection of unusual activity that could pose compliance risks. The dashboard's real-time features support the proactive monitoring required by EU directives, even in cases where simplified due diligence applies to low-value transactions.

Using Flash Lightning Network for Compliant Transactions

Flash also integrates the Lightning Network to enhance compliance while ensuring efficiency. This integration allows for instant, low-cost transactions while maintaining AML oversight. EU AML directives acknowledge that "new technologies provide time-effective and cost-effective solutions" and encourage their use to combat money laundering. The Lightning Network's structure enables Flash to facilitate seamless settlements without the need for payout requests, simplifying cash flow and reducing the complexity of audits.

The directive's Simplified Due Diligence (SDD) provisions are particularly relevant for Lightning Network micro-payments. In low-risk scenarios - such as small transactions used solely for purchasing goods or services - certain customer due diligence measures may be waived. However, even with these exemptions, the directive requires ongoing "monitoring of transactions or of business relationships" to prevent misuse of AML rules. Flash's real-time monitoring tools ensure this oversight remains active while preserving the speed and efficiency that make Lightning Network transactions appealing.

Building Risk-Based AML Strategies with Flash

Flash takes its anti-money laundering (AML) compliance tools to the next level by enabling businesses to implement risk-based strategies that improve operational oversight and efficiency.

Automated Screening and Analytics with the Flash Dashboard

Flash's dashboard automates risk screening, eliminating the need for manual compliance checks. It continuously monitors customers and transactions against global watchlists, including sanctions lists, Politically Exposed Persons (PEPs), and adverse media sources, as transactions occur. This automation significantly reduces investigation times, allowing analysts to focus on genuine threats instead of wasting time on false positives.

The dashboard also includes behavioral analytics that monitor transaction patterns to detect unusual activity early. For instance, if a customer suddenly increases their transaction volume or moves funds in unexpected ways, the system updates their risk profile automatically. Consider this: in 2024, cryptocurrency fraud in the U.S. resulted in $9.3 billion in losses - a staggering 66% jump from the previous year. Flash’s analytics also extend to blockchain tracing, tracking funds across multiple addresses to uncover attempts to hide illicit activity. With only 0.34% of cryptocurrency activity linked to illicit use in 2023, tools like these help legitimate businesses operate securely without being overwhelmed by false alarms. These capabilities build on Flash’s existing compliance framework, addressing the unique challenges faced by Bitcoin payment gateways and other crypto platforms.

While automated analytics handle real-time risk assessments, Flash also offers custom integrations to consolidate and streamline compliance workflows.

Custom Integrations for Better Compliance Management

Flash provides custom integrations that bring all compliance processes into a single, unified system. Instead of juggling separate tools for tasks like KYC verification, sanctions screening, and wallet monitoring, businesses can manage everything from one platform. Every compliance interaction updates a customer's risk score in real time, eliminating data duplication and reducing alert fatigue.

"The more your analysts have to switch between tabs, the more risk you are introducing." – KYC-Chain

These integrations allow businesses to tailor automation to their specific risk profiles. Low-risk customers can be onboarded in seconds using automated workflows, while high-risk cases are flagged for senior analysts to perform enhanced due diligence. This approach helps mitigate the risks of inadequate AML programs, especially as crypto companies faced over $5.1 billion in fines in 2024 alone. By scaling compliance processes to match transaction growth without compromising quality, Flash’s integration capabilities ensure businesses maintain robust oversight and avoid costly penalties.

Conclusion

AML directives are reshaping the way Bitcoin payment gateways operate. With regulations like the FATF Travel Rule, the US Bank Secrecy Act, and evolving EU frameworks, compliance requirements have become more demanding. These include customer due diligence, transaction monitoring, and rigorous reporting protocols. The stakes are high - cryptocurrency fraud losses in the US reached a staggering $9.3 billion in 2024, while crypto companies faced fines exceeding $5.1 billion in the same year.

Meeting these challenges requires efficient, technology-driven compliance measures. Flash addresses these needs with innovative tools and a wallet-to-wallet model that ensures transparency while maintaining a non-custodial structure. Its real-time monitoring features automatically screen transactions against global watchlists and flag suspicious activity, such as structuring or layering. Additionally, Flash's blockchain analytics trace the origins of funds across multiple addresses, helping businesses align with the growing regulatory focus on fostering a "duty of care" culture. By offering custom integrations, it brings together KYC verification, sanctions screening, and wallet monitoring into a single, streamlined system.

Industry experts acknowledge the value of prioritizing compliance:

"Complying with financial regulation takes time and money, and businesses that have historically invested in compliance resources will have a significant head start." – David Carlisle, Director of Policy and Regulatory Affairs, Elliptic

As regulators push for harmonized AML standards and stricter classifications for VASPs, scalable solutions are becoming indispensable. Flash's risk-based approach automates low-risk tasks while flagging high-risk cases, ensuring compliance without slowing down transactions.

For businesses aiming to accept Bitcoin payments while staying compliant with AML regulations, Flash offers the tools, automation, and analytics necessary to navigate the complexities of today's regulatory environment.

FAQs

How do AML directives affect the costs and operations of Bitcoin payment gateways?

AML directives play a major role in shaping the expenses and day-to-day operations of Bitcoin payment gateways. To meet these regulatory demands, businesses need to establish thorough systems for verifying user identities, monitoring transactions, and submitting necessary reports. These measures often require significant investment in compliance tools, obtaining and maintaining licenses, and keeping up with changing regulations.

Failing to comply can lead to hefty fines and damage to a company’s reputation, making it crucial for businesses to prioritize adherence. Although compliance introduces additional layers of complexity, it also fosters trust and ensures businesses can function within legal boundaries - especially in regions like the U.S., where AML regulations are particularly stringent.

What challenges do unhosted wallets and mixing services create for AML compliance?

Unhosted wallets and mixing services present challenges for Anti-Money Laundering (AML) compliance because they enable users to maintain a high degree of privacy and anonymity. This level of concealment makes it harder to trace where transactions originate or to identify any potentially illegal activities.

By obscuring transaction histories, these tools create significant hurdles for businesses and regulators working to enforce AML regulations. To address these risks, companies need to adopt strong monitoring systems and verification processes to remain compliant with legal standards while managing these complexities.

How is the FATF Travel Rule applied differently around the world?

The FATF Travel Rule is implemented differently worldwide, largely due to variations in local laws and how enforcement is handled. While the FATF sets a global standard for applying the rule to virtual asset service providers (VASPs), individual countries tailor it to fit their specific legal systems. Take the United States, for instance - agencies like FinCEN enforce the rule with defined thresholds and clear compliance guidelines. In contrast, other regions might have less strict or still-developing regulations.

One major difference lies in the transaction reporting threshold. The FATF recommends a $1,000 threshold for virtual asset transactions, but how this is enforced differs. Some nations opt for tighter thresholds, while others are more relaxed, making cross-border compliance tricky. For crypto businesses, understanding these regional nuances is critical to ensuring compliance and avoiding fines.