Accepting Bitcoin as payment in Australia comes with specific tax and regulatory obligations. Here's what you need to know:

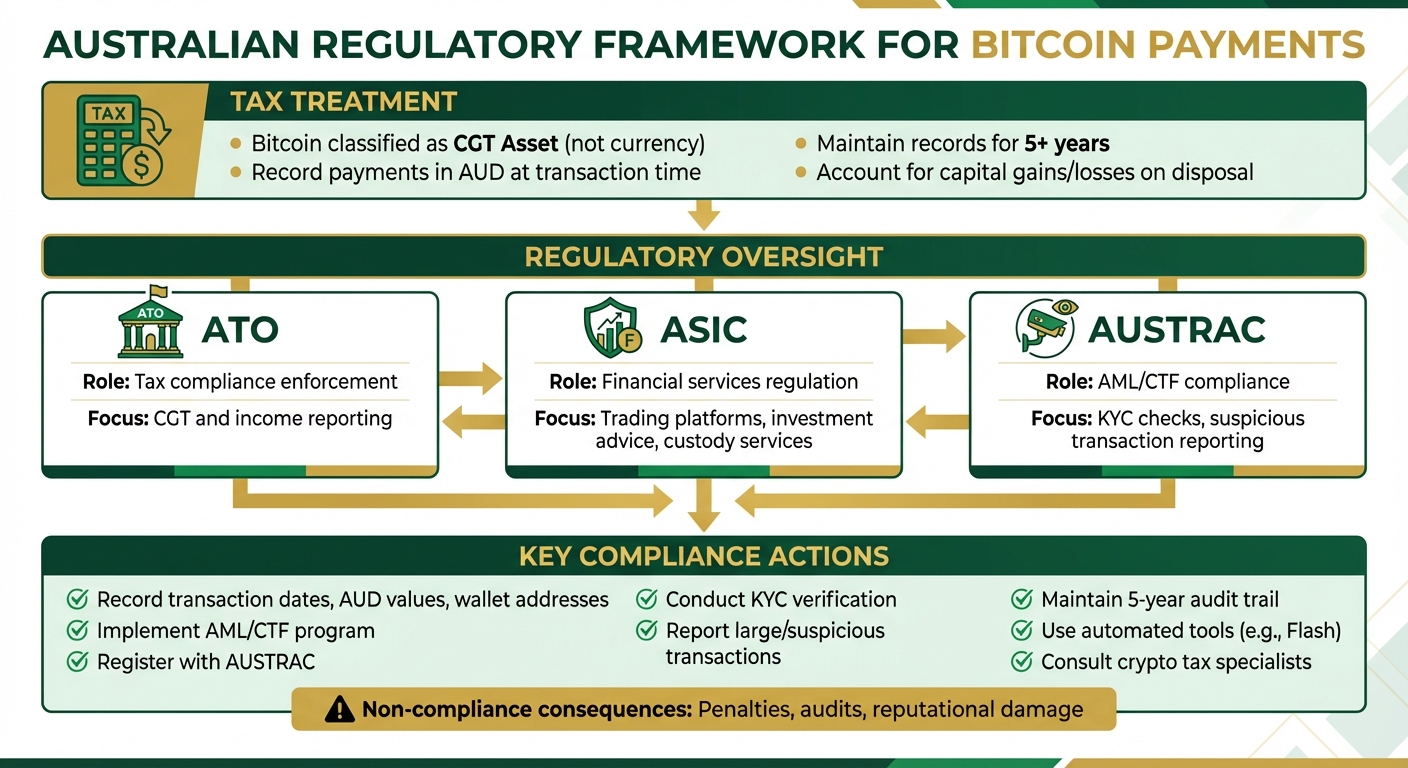

- Tax Treatment: The Australian Taxation Office (ATO) classifies Bitcoin as a Capital Gains Tax (CGT) asset, not as currency. Businesses must:

- Record Bitcoin payments in Australian dollars (AUD) at the transaction time.

- Maintain detailed transaction records for at least five years.

- Account for capital gains or losses when Bitcoin is sold, traded, or used.

- Regulatory Oversight:

- ATO: Enforces tax compliance for Bitcoin transactions.

- ASIC: Regulates financial services involving Bitcoin, like trading platforms or investment advice.

- AUSTRAC: Requires businesses to follow Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) rules, including Know Your Customer (KYC) checks and reporting large or suspicious transactions.

- Compliance Tips:

- Use tools like Flash for automated record-keeping and reconciliation.

- Regularly review tax filings and AML/CTF procedures.

- Consult crypto tax specialists to navigate complex regulations.

Failing to comply can result in penalties, audits, and reputational harm. Staying organized, maintaining accurate records, and leveraging automation tools can help businesses manage Bitcoin payments effectively.

Australian Bitcoin Payment Compliance: Tax and Regulatory Framework Overview

Tax Rules for Bitcoin Payments in Australia

How the ATO Classifies Bitcoin

The Australian Taxation Office (ATO) treats Bitcoin as property and a Capital Gains Tax (CGT) asset, similar to shares or investment properties - not as money or foreign currency. This classification determines how businesses need to handle and report income from Bitcoin transactions.

Recording Income from Bitcoin Payments

If your business accepts Bitcoin as payment for goods or services, you must calculate its market value in Australian dollars (AUD) at the time of the transaction. This value should then be recorded as ordinary business income. For businesses registered for GST, the GST amount must be calculated based on the AUD value.

To stay compliant, keep detailed records for at least five years. These records should include:

- Dates of transactions

- Market value in AUD

- Parties involved

- Wallet addresses

- Quantities and unit prices

- Any associated fees

Accurate records are not just a legal requirement - they're also crucial for understanding how CGT applies when you dispose of Bitcoin.

Capital Gains Tax on Bitcoin Transactions

A CGT event occurs whenever you dispose of Bitcoin. This includes selling it for AUD, trading it for another cryptocurrency, or using it to pay for goods or services. The capital gain or loss is calculated by comparing the disposal value (in AUD) with your cost basis, which includes the original purchase price and any fees.

To avoid double taxation, any amount already recorded as ordinary income is deducted from the capital gain. For instance, if you recorded $10,000 worth of Bitcoin as income and later sold it for $12,000, only the $2,000 gain would be subject to CGT.

Additionally, if you use Bitcoin to purchase business-related items, you may be eligible for tax deductions. These deductions are based on the arm's length value of the purchased items.

🔥New CRYPTO TAX Rules in Australia | Is Bitcoin MONEY? | Capital Gains vs Income Laws 2025 Guide

Regulatory Requirements and Reporting Standards

This section dives into the regulatory and reporting standards that govern Bitcoin payments in Australia, building on the tax obligations discussed earlier.

ASIC Requirements for Financial Services

Australia doesn’t have a single, overarching cryptocurrency law. Instead, businesses must navigate regulations from ASIC, AUSTRAC, and the ATO. The focus of regulation here is less about the technology itself and more about how businesses operate.

ASIC determines whether Bitcoin-related activities fall under financial services. For example, if your business offers Bitcoin investment advice, operates a trading platform, or provides custody services, you might need an Australian Financial Services (AFS) license. However, if you’re simply accepting Bitcoin as payment for goods or services, ASIC licensing typically won’t apply. That said, it’s crucial to assess your specific activities against ASIC’s guidelines.

In addition to ASIC’s role, AUSTRAC enforces rules aimed at monitoring transactions and preventing fraud.

AUSTRAC and Anti-Money Laundering Rules

If your business accepts Bitcoin, you are required to implement an AML/CTF program. This includes registering with AUSTRAC and adhering to strict customer verification rules. Key steps include:

- Conducting Know Your Customer (KYC) checks.

- Monitoring for suspicious activities.

- Reporting transactions that exceed certain thresholds.

These requirements apply regardless of the size of your business. For example, you’ll need to flag unusual transaction patterns, large transfers, or behaviors that seem inconsistent with a customer’s normal activity. Non-compliance can lead to hefty penalties and damage to your reputation.

Record-Keeping Requirements from the ATO

In addition to the transaction details mentioned earlier, the ATO mandates that businesses maintain records like digital wallet logs, private keys, exchange transactions, and even professional fees related to Bitcoin activities for at least five years. These documents are critical for audits.

"The ATO is here to help those that are genuinely trying to meet their tax obligations. However, where people attempt to deliberately avoid these obligations, we will take strong action." - ATO spokesperson

If you notice errors in your tax filings, it’s best to contact the ATO immediately. Voluntarily disclosing mistakes before an audit begins can significantly reduce penalties. For businesses handling complex Bitcoin transactions, consulting a registered tax agent or crypto tax specialist is a smart move to ensure compliance and accurate reporting.

sbb-itb-f81ab9b

Managing Bitcoin Transactions and Accounting

Keeping track of Bitcoin payments and maintaining precise financial records requires a structured approach. This includes properly classifying Bitcoin in your accounts, reconciling transactions, and using tools that help ensure compliance. Building on the earlier discussion about regulations, this section dives into practical steps for managing Bitcoin transactions and accounting.

How to Account for Bitcoin in Financial Statements

Since the ATO classifies Bitcoin as an asset, your financial records should reflect this. When you receive Bitcoin, record it as an asset at its AUD market value at the time of receipt. This value becomes the cost basis for calculating capital gains tax (CGT).

For instance, if you receive 0.05 BTC when the market price is $100,000 AUD, you would record $5,000 AUD as revenue. Later, if you convert that Bitcoin when the price rises to $110,000 AUD, the $500 AUD difference is a capital gain and subject to CGT. Your financial statements should clearly separate Bitcoin holdings from other assets and include details about the valuation method used.

Tracking and Reconciling Bitcoin Transactions

Reconciliation involves ensuring your internal transaction records align with the blockchain ledger. This means comparing details like transaction dates, amounts, and IDs from your accounting system with those recorded on the blockchain. You’ll also need to account for network fees or any adjustments.

Challenges here can include managing multiple wallets, dealing with a high volume of transactions, and navigating price fluctuations. To stay organized, establish a regular schedule for reconciliation, document the steps in your process, and set up alerts for significant transactions. This helps ensure your records remain accurate and up to date.

Using Flash for Compliance Management

Flash simplifies the complexities of Bitcoin accounting with features like real-time analytics and automated invoicing. As payments are received, Flash automatically records transaction details - timestamps, amounts in both BTC and AUD, and customer information - creating a clear audit trail that aligns with ATO record-keeping requirements.

Since Flash operates on the Lightning Network, transactions settle instantly. Its dashboard offers immediate visibility into your Bitcoin revenue, making reconciliation much easier. You can directly compare Flash’s transaction logs to the blockchain without needing manual data entry. Additionally, Flash integrates with your existing financial systems, streamlining compliance and simplifying your workflow.

Risk Management and Compliance Controls

Accepting Bitcoin payments comes with its share of compliance hurdles that demand careful attention. The Australian Taxation Office (ATO) closely monitors crypto transactions through data-matching programs with both domestic and international exchanges, making non-reporting a risky choice. Poor record-keeping can heighten the risk of audits. Additionally, the unique traits of cryptocurrencies - such as their speed, global accessibility, and potential for anonymity - make them appealing for unlawful activities like money laundering and terrorism financing.

Common Compliance Risks to Address

Beyond meeting regulatory requirements, businesses must tackle specific compliance risks tied to cryptocurrency. For example, misclassifying your business as an investor rather than a trader - or vice versa - can result in hefty tax obligations. Weak Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) controls can also lead to financial penalties and harm your reputation. Investors typically face Capital Gains Tax (CGT) and may qualify for a 50% discount if assets are held for more than 12 months. On the other hand, traders are taxed at full marginal income rates without access to the CGT discount.

Building Internal Policies for Bitcoin Payments

Developing clear internal policies is a critical step when handling Bitcoin payments. These policies should include key details such as transaction dates and times, their value in AUD, customer information, wallet addresses, and transaction IDs. Assign specific reconciliation responsibilities within your team and conduct regular reviews of your records. Strong internal policies provide the groundwork for managing compliance effectively.

Action Steps for CFOs

To navigate these challenges, CFOs can take the following steps:

- Clarify your ATO classification: Determine whether your business operates as an investor or trader, as this will influence your tax obligations.

- Implement automated systems: Use tools like Flash for automated invoicing and real-time analytics to ensure every transaction detail is accurately captured. These systems reduce manual errors and help maintain a complete audit trail that aligns with ATO expectations.

- Schedule quarterly compliance reviews: Regularly check that your record-keeping practices meet ATO standards and update your AML/CTF procedures as needed. Train your finance team on the unique tax rules surrounding crypto, as most crypto transactions - including sales, swaps, purchases, gifts, or earned rewards - are taxable events.

- Work with crypto tax experts: Build relationships with advisors who specialize in cryptocurrency taxation and compliance. Their expertise can help you stay ahead of regulatory changes and adapt your policies to evolving digital asset guidelines.

Conclusion

Accepting Bitcoin payments in Australia comes with a web of tax and regulatory responsibilities. When you receive Bitcoin payments, they must be recorded at their AUD value at the time of receipt and treated as taxable income, which triggers specific tax obligations. The Australian Taxation Office (ATO) uses an advanced data-matching system to track crypto transactions from exchanges, with records going back to 2014. This makes accurate and timely reporting absolutely essential. But taxes are just one piece of the puzzle.

You also need to meet AUSTRAC's anti-money laundering and counter-terrorism financing (AML/CTF) requirements, as well as follow relevant guidelines set by the Australian Securities and Investments Commission (ASIC). The regulatory environment for digital assets in Australia is constantly evolving. The government is working on comprehensive frameworks that address licensing, custodial standards, and consumer protection. Meanwhile, ASIC’s 2024–28 Corporate Plan emphasizes tackling technology-enabled misconduct as a top enforcement priority.

In this shifting landscape, keeping detailed records is your strongest safeguard. Be sure to maintain thorough records for at least five years. Automated tools like Flash can simplify this process by capturing transaction data in real-time and creating complete audit trails. Additionally, consulting with crypto tax specialists can help your business stay ahead of regulatory changes and reduce compliance risks.

FAQs

What are the main tax considerations for businesses in Australia accepting Bitcoin payments?

Businesses in Australia that accept Bitcoin need to understand its tax implications. The Australian Taxation Office (ATO) classifies Bitcoin as property for tax purposes, which means it falls under capital gains tax (CGT) when disposed of. This can happen through selling, trading, gifting, converting it to fiat currency, or even using it to make purchases. To stay compliant, businesses must keep detailed records of every transaction.

When Bitcoin is used in business activities, transactions might also attract Goods and Services Tax (GST). Income generated from Bitcoin mining is considered taxable, but the good news is that associated expenses can be deducted. Moreover, if Bitcoin is held for more than 12 months, businesses may qualify for a 50% CGT discount. Failing to meet these obligations could lead to penalties or audits by the ATO.

To reduce potential risks, focus on maintaining precise records, leverage reliable tracking tools, and seek advice from tax professionals who specialize in cryptocurrency regulations in Australia.

What steps can businesses take to meet AUSTRAC's AML/CTF requirements when accepting Bitcoin payments?

To meet AUSTRAC's AML/CTF requirements when dealing with Bitcoin payments, businesses need to establish a thorough compliance program. Key steps include verifying customer identities through Know Your Customer (KYC) procedures, keeping an eye on transactions to spot anything unusual or suspicious, and promptly reporting significant or suspicious activity to AUSTRAC.

On top of that, businesses must register with AUSTRAC before offering their services. They’re also required to keep detailed transaction records and ensure their staff receives regular compliance training. These measures not only align with Australian regulations but also help reduce potential risks tied to Bitcoin payments.

How can businesses properly track and report Bitcoin transactions for tax purposes?

To ensure compliance, businesses need to keep thorough records of all Bitcoin transactions. This includes documenting the date, the amount in USD, transaction fees, and the parties involved in each transaction. For tax purposes, calculating capital gains or losses requires comparing the transaction value to the original purchase price.

Activities such as sales, trades, or conversions must be reported on tax returns, with records preserved for at least five years. Leveraging reliable crypto tracking tools can make this process easier by generating accurate, tax-compliant reports. Staying organized and ahead of deadlines helps reduce compliance risks and keeps reporting hassle-free.