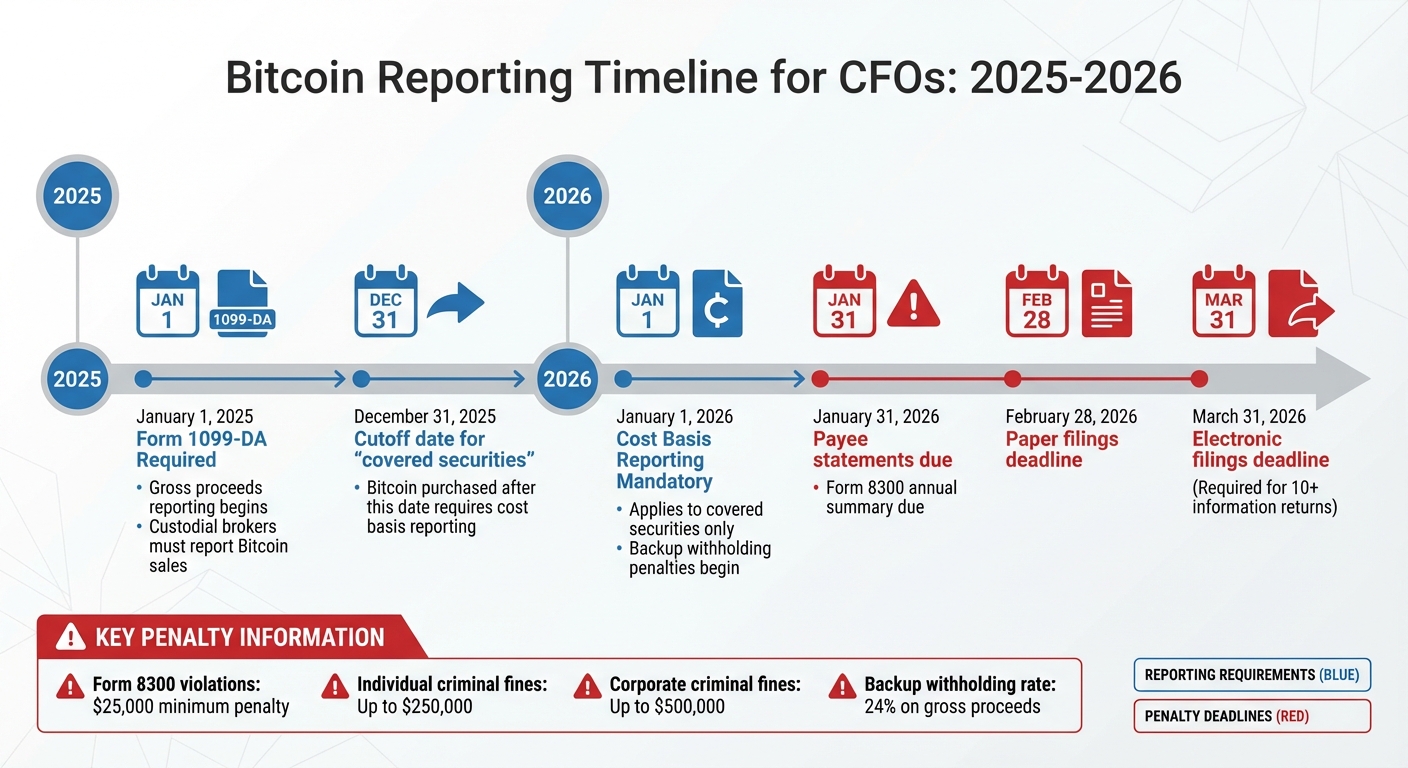

Bitcoin’s increasing presence in corporate finances has introduced complex IRS reporting requirements. Starting in 2025, custodial brokers must report Bitcoin sales on Form 1099-DA, with cost basis reporting mandatory by 2026. Every transaction - buying, selling, or using Bitcoin - triggers taxable events, requiring meticulous documentation of fair market value, cost basis, and transaction details.

Key challenges include handling Bitcoin’s price volatility, choosing between FIFO or specific identification for reporting, and accurately categorizing fees and unique activities like mining or staking. Non-compliance risks penalties, including fines up to $500,000 for corporations. Automation tools, like Flash, simplify compliance by tracking transactions, calculating FMV, and maintaining audit-ready records.

Deadlines to note:

- January 31, 2026: Payee statements due.

- February 28, 2026: Paper filings due.

- March 31, 2026: Electronic filings due.

Staying ahead means understanding IRS rules, maintaining precise records, and leveraging automated solutions to meet reporting obligations.

Bitcoin IRS Reporting Deadlines and Requirements 2025-2026

Digital Assets Are Entering the Compliance Era

IRS Reporting Requirements for Bitcoin Transactions

The IRS has rolled out a phased plan for digital asset reporting, which directly affects how CFOs manage Bitcoin transactions. Staying compliant with these rules is crucial to avoid potential penalties.

Form 1099-DA Requirements

Starting January 1, 2025, brokers will need to report gross proceeds from Bitcoin sales on Form 1099-DA. By January 1, 2026, they’ll also need to include the cost basis for "covered securities." This applies to Bitcoin purchased in a custodial account after December 31, 2025. However, Bitcoin acquired before 2026 or transferred from an external wallet is considered "noncovered" and doesn’t require basis reporting.

For the 2025 tax year, the IRS has stated it won’t penalize brokers for incorrect or late Form 1099-DA filings if they can demonstrate good faith efforts to comply. To minimize the risk of backup withholding penalties starting in 2026, brokers are encouraged to verify customer tax identification numbers using the IRS TIN-matching program.

Understanding who qualifies as a broker under these rules is the next step in navigating these requirements.

Who Qualifies as a Broker Under IRS Rules

The IRS defines a broker as anyone who regularly facilitates digital asset sales for others. This includes custodial digital asset trading platforms, hosted wallet providers, digital asset kiosks, and certain processors of digital asset payments (PDAPs). Identifying whether you fall under this definition is critical for determining your reporting responsibilities.

Entities that strictly provide mining or validation services - or those offering hardware and software that allow users to manage their private keys without additional services - are excluded from broker status.

In July 2025, the IRS revoked a proposed rule that would have required DeFi participants to report as brokers. As it stands, non-custodial platforms currently have no reporting obligations under these regulations.

How to Keep Accurate Bitcoin Transaction Records

Keeping precise Bitcoin transaction records isn't just a good habit - it's essential for staying compliant with IRS rules and aligning your data with publicly available IRS blockchain records. Since the IRS treats Bitcoin as property rather than currency, you’ll need detailed documentation to withstand potential audits.

Required Transaction Details to Document

For every transaction, you should record the following:

- Date and time of the transaction.

- Number of Bitcoin units involved.

- Fair Market Value (FMV) in U.S. dollars at the time of the transaction.

- Cost basis, which includes the purchase price along with any commissions, transaction fees, or gas fees.

When disposing of Bitcoin, you’ll also need to calculate and document the "amount realized." This is determined by adding the cash received and the FMV of any property or services, then subtracting transaction costs like transfer taxes or platform fees.

If you decide not to use the default First-In, First-Out (FIFO) accounting method, you’ll need to maintain detailed records that include unique digital identifiers, such as private keys, public keys, or wallet addresses, for each Bitcoin unit. Without this level of precision, the IRS will default to FIFO or, in the case of undocumented gifted assets, may assume a cost basis of zero.

"The Internal Revenue Code and regulations require taxpayers to maintain sufficient records to establish the positions taken on federal income tax returns." - Internal Revenue Service

Using Automation for Transaction Tracking

Automation can make tracking Bitcoin transactions much easier. Automated tools can capture FMV at the exact timestamp of a transaction using trusted blockchain explorers. These systems also standardize accounting methods, whether you’re using FIFO, Highest-In First-Out (HIFO), or specific lot selection.

Another advantage of automation is its ability to differentiate taxable events, like receiving Bitcoin as payment for services, from non-taxable internal transfers. By integrating blockchain explorer data into your accounting system, you can automatically log transaction costs - such as gas fees - ensuring accurate calculations of your adjusted basis and any capital gains or losses.

These automated records not only simplify your tracking process but also make it easier to compare your records with IRS blockchain data, as explained below.

Matching Records with IRS Blockchain Data

Once you’ve implemented automated tracking, it’s vital to ensure your records align with IRS blockchain data. The IRS has independent access to blockchain records, so your internal logs must match their data. On-chain transactions are valued at the time they’re recorded on the blockchain, while off-chain transactions should be valued as if they were recorded on-chain at the same time.

Starting in 2026, brokers will be required to report cost basis for covered securities on Form 1099-DA. To prepare for this, it’s a good idea to regularly reconcile your records with broker statements. This allows you to catch and fix discrepancies before filing your taxes. Additionally, Revenue Procedure 2024-28 outlines how to allocate unused basis to digital assets held in wallets or accounts as of January 1, 2025. Make sure to document wallet-to-wallet transfers to prove ownership hasn’t changed, as this information will be required for accurate reporting on information returns.

sbb-itb-f81ab9b

Filing Deadlines and Penalties for Bitcoin Reporting

When to File Bitcoin Reporting Forms

The IRS has set clear deadlines for reporting digital asset transactions. Starting January 1, 2025, all such transactions must be reported using Form 1099-DA, with the first set of reports due in early 2026. Brokers are required to provide payee statements by January 31 of the year following the transaction. Paper filings must be submitted by February 28, while electronic filings have a later deadline of March 31. If your organization files 10 or more information returns (including forms like 1099s and W-2s) in a single calendar year, you must file electronically.

If your business receives over $10,000 in cash or digital assets, Form 8300 must be filed within 15 days of the transaction. Additionally, an annual summary statement must be sent to the recipient by January 31 of the following year. For CFOs managing Widely Held Fixed Investment Trusts (WHFITs), the tax information statement for 2025 must be provided to trust interest holders no later than March 16, 2026.

Meeting these deadlines is essential to avoid the penalties outlined below.

Financial Penalties for Late or Incorrect Filing

Failing to file accurate or timely reports can lead to hefty penalties. Under IRC §§ 6721 and 6722, incorrect or late information returns can result in large fines, along with potential backup withholding if Taxpayer Identification Numbers (TINs) are not verified. For Form 8300 violations, intentional or willful disregard of the reporting rules carries a minimum penalty of $25,000, with criminal fines reaching up to $250,000 for individuals and $500,000 for corporations.

However, there is some relief for the 2025 calendar year. If you can demonstrate that your reporting efforts were made in good faith and are supported by thorough records, penalties may be waived. To reduce the risk of backup withholding penalties, consider using the IRS TIN-matching program.

For Bitcoin acquired before January 1, 2026 (classified as noncovered securities), checking Box 9 on Form 1099-DA can shield your organization from penalties related to incorrect basis or acquisition date information. If Box 9 is left unchecked, you will remain fully liable for those penalties.

Using Flash for Compliant Bitcoin Payments

Navigating the IRS's strict guidelines for Bitcoin transactions can be tricky, but Flash offers solutions that tackle these challenges head-on. By focusing on precise, automated record-keeping, Flash delivers payment tools designed to simplify compliance.

Flash's Wallet-to-Wallet Payment System

Flash operates through a non-custodial system, enabling direct wallet-to-wallet transfers. This setup ensures a transparent audit trail by recording funds as they move between wallets. Each transaction logs the fair market value (FMV) at the time it occurs, meeting IRS documentation standards. CFOs can easily access detailed transaction histories that align with compliance requirements.

Lightning Network Integration for Instant Transactions

Flash brings Lightning Network support into the mix, allowing off-chain Bitcoin transactions that settle instantly. These transactions bypass traditional exchanges, reducing costs while maintaining the detailed records needed for tax reporting.

The system timestamps and logs USD values for every transaction, making it easier to identify specific Bitcoin units used, along with their purchase date, time, and price. This feature is crucial for meeting the IRS's cost basis reporting requirements, which become mandatory starting January 1, 2026. By automating these processes, Flash helps streamline compliance and simplifies reporting.

How Flash Simplifies Bitcoin Reporting for CFOs

Flash takes the headache out of Bitcoin accounting by automating essential tasks. The platform organizes transactions at the individual wallet level, addressing the IRS's requirement to trace specific digital assets from acquisition to disposition. This eliminates reliance on the outdated "universal wallet" concept.

For transactions under the $600 de minimis threshold, Flash reduces unnecessary reporting burdens. Since transactions below this amount don't need to be reported by processors of digital asset payments, CFOs can save time and effort. Additionally, Flash tracks transaction costs like Lightning Network fees, which can either reduce the amount realized or increase the adjusted basis on tax returns. This is especially helpful for CFOs managing numerous small transactions, ensuring compliance without drowning in paperwork.

Conclusion

CFOs handling Bitcoin transactions are navigating a landscape of evolving compliance requirements that demand precision and attention to detail. The IRS classifies digital assets as property, which means businesses must address mandatory disclosure questions on their corporate tax returns.

Key reporting deadlines are approaching fast: gross proceeds reporting takes effect on January 1, 2025, while cost basis reporting begins January 1, 2026. To stay compliant, businesses need to identify specific Bitcoin units, automate fair market value tracking, and maintain detailed records, including transaction costs like network fees. Without proper documentation, the default FIFO (First In, First Out) method applies, which could lead to higher tax liabilities. Inaccurate reporting can result in financial penalties, interest charges, and a 24% backup withholding rate on gross proceeds.

Flash’s wallet-to-wallet payment system simplifies compliance by automating record-keeping, providing real-time USD valuations, and maintaining audit-ready transaction histories. This transforms what was once a tedious manual process into an efficient, streamlined operation.

As regulations tighten, CFOs must adapt their strategies to keep pace. The regulatory focus is shifting from creating rules to ensuring they are applied in practice. Perry Woodin, CEO of NODE40, emphasized this shift:

"2026 is about making [rules] work in real compliance and real audits. The shift is moving from regulation to operations".

FAQs

How can CFOs prepare for the 2026 cost basis reporting requirements for Bitcoin?

CFOs need to keep a close eye on IRS regulations surrounding digital assets, especially as the 2026 cost basis reporting requirements approach. A key step is maintaining precise and thorough records of all Bitcoin transactions - this includes tracking dates, transaction amounts, and cost basis details.

To get ahead, review the latest IRS guidelines on reporting virtual currencies and establish systems to capture all necessary data. Collaborating with tax professionals can also be a smart move to ensure your organization is ready for these changes and stays compliant with any regulatory updates.

How can Flash help businesses manage Bitcoin transaction records for IRS compliance?

Flash takes the hassle out of managing Bitcoin transaction records for IRS compliance by automating essential tasks like tracking and reporting. Since IRS regulations demand thorough documentation of digital asset transactions, Flash steps in to capture and organize transaction data in real-time. This not only minimizes errors but also ensures the information is accurate and up-to-date. Plus, its non-custodial wallet-to-wallet system enables instant payments, making it simple to monitor transactions as they occur.

On top of that, Flash can produce detailed reports tailored to IRS requirements, helping businesses stay on top of compliance with minimal effort. It integrates smoothly with accounting systems, ensuring all transaction details are properly logged and easily accessible for audits. This reduces administrative burdens and makes compliance far less complicated.

What happens if a business doesn’t follow the new Bitcoin reporting requirements?

Failing to follow the updated Bitcoin reporting rules can bring about serious penalties and increased attention from tax authorities. These rules aim to improve transparency and ensure accurate tax reporting for digital asset transactions.

Ignoring these requirements could lead to fines, legal troubles, or even audits, which might create challenges for your business operations. It's crucial to stay informed and comply with these regulations to steer clear of avoidable risks and stay aligned with U.S. tax laws.