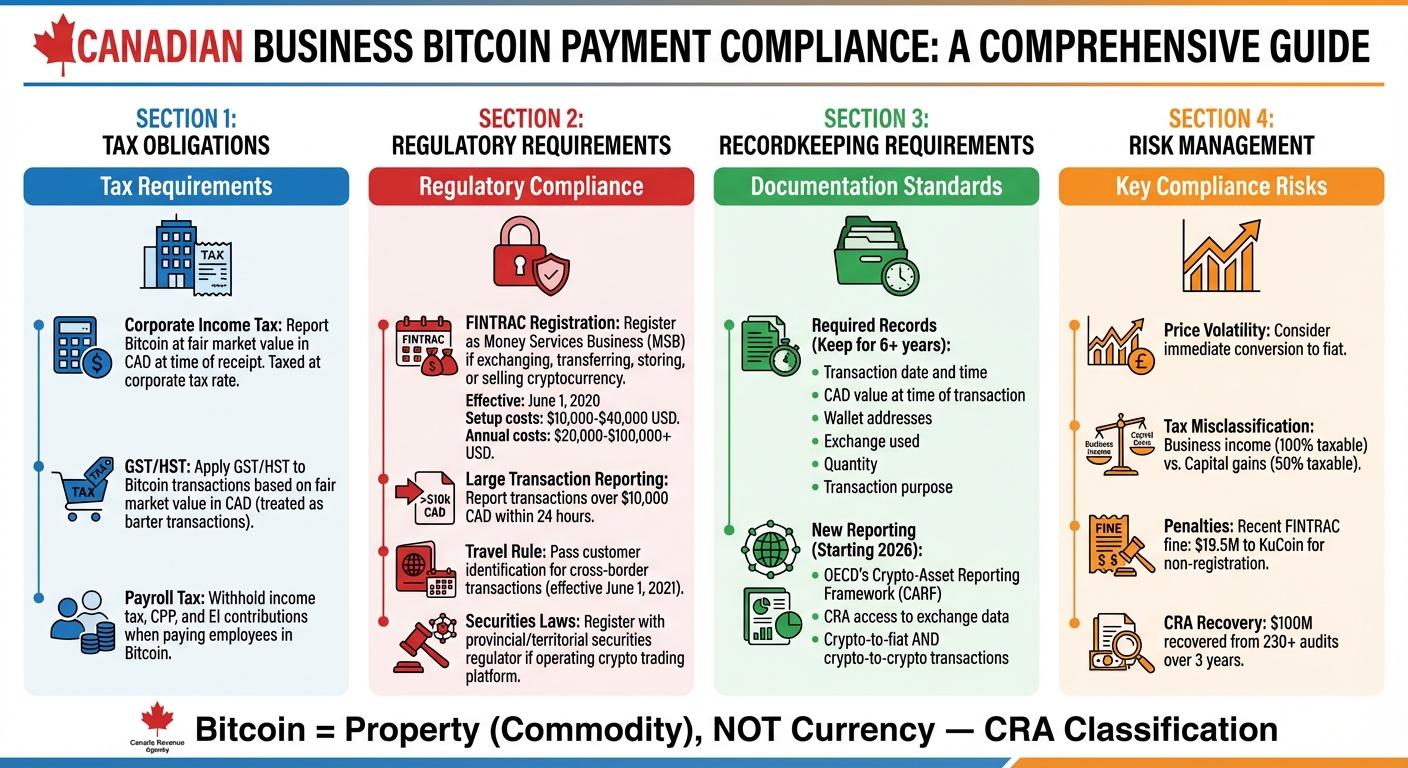

If you're a business in Canada accepting Bitcoin, you need to understand the tax and regulatory rules to stay compliant. Here's the key takeaway: Bitcoin is treated as property, not currency, by the Canada Revenue Agency (CRA). This means every Bitcoin transaction is considered a barter transaction, requiring careful recordkeeping and adherence to tax and anti-money laundering (AML) laws.

Key Points to Know:

- Tax Obligations:

- Report Bitcoin income at its fair market value in CAD at the time of the transaction.

- GST/HST applies to Bitcoin transactions for taxable goods or services.

- Paying employees in Bitcoin requires withholding income tax, CPP, and EI contributions.

- Regulatory Requirements:

- Businesses dealing with cryptocurrency must comply with FINTRAC's AML laws, which include registering as a Money Services Business (MSB) if applicable.

- Large transactions (over CAD $10,000) must be reported within 24 hours.

- Securities laws may apply if your business involves crypto trading platforms or Initial Coin Offerings (ICOs).

- Recordkeeping:

- Keep detailed records of transaction dates, CAD values, wallet addresses, and purposes for at least six years.

- Starting in 2026, the CRA will have access to more crypto transaction data under the OECD's Crypto-Asset Reporting Framework (CARF).

- Risk Management:

- Bitcoin's price volatility can impact your business. Consider converting Bitcoin to fiat immediately to reduce risks.

- Misclassifying Bitcoin income (e.g., as capital gains instead of business income) can lead to penalties.

To simplify compliance, tools like Flash offer wallet-to-wallet payment solutions that automate recordkeeping and ensure transactions meet CRA standards.

Bottom Line: Businesses must navigate complex tax and regulatory frameworks when accepting Bitcoin. Proper recordkeeping, understanding your obligations, and using compliant tools can help you avoid penalties and operate smoothly.

Canadian Bitcoin Payment Compliance Requirements for Businesses

How Canadian Crypto Taxes Work in 2025 - A Simple Guide

Tax Requirements for Bitcoin Payments

If you're a Canadian business accepting Bitcoin, it's crucial to understand how the Canada Revenue Agency (CRA) handles tax obligations. Here's a breakdown of what you need to know about corporate income, sales, and payroll taxes when dealing with Bitcoin.

Corporate Income Tax on Bitcoin Transactions

Income from Bitcoin payments is taxed at your corporate tax rate, as per CRA guidelines. If your business regularly deals with cryptocurrency, these transactions are considered part of your regular operations. To comply, you must report the fair market value of Bitcoin in Canadian dollars (CAD) at the time of receipt. For example, if you receive 0.05 BTC and its value is $3,000 CAD, you need to record that amount as business income. The CRA emphasizes using the fair market value at the transaction time to ensure accurate reporting.

Sales Tax on Bitcoin Payments

Bitcoin transactions are subject to GST/HST rules, just like traditional payments. When you accept Bitcoin for taxable goods or services, you must calculate and remit GST/HST based on the transaction's fair market value in CAD. Since the CRA treats cryptocurrency payments as barter transactions, you need to determine the GST/HST owed for each sale. Keeping detailed records - such as dates, amounts, and transaction values in CAD - will help ensure accurate GST/HST reporting.

Payroll Tax for Bitcoin Compensation

Paying employees or contractors in Bitcoin comes with specific tax responsibilities. The CRA views these payments as barter transactions for income tax purposes. You must record the fair market value of Bitcoin in CAD at the time of payment. For employees, Bitcoin compensation is treated as employment income, meaning you must withhold income tax, Canada Pension Plan (CPP) contributions, and Employment Insurance (EI) premiums as required.

Regulatory Requirements for Businesses

In Canada, businesses accepting Bitcoin must navigate a complex set of regulatory requirements beyond just tax obligations. These rules are in place to combat financial crimes and uphold the integrity of the financial system, regardless of transaction size. Below, we’ll break down key areas like anti-money laundering (AML) measures, securities regulations, and payment processing rules to help you stay compliant.

Anti-Money Laundering (AML) Requirements

The Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) plays a central role in enforcing AML and anti-terrorist financing laws for businesses involved in virtual currencies. If your business exchanges, transfers, stores, or sells cryptocurrency on behalf of clients, you’re required to register as a Money Services Business (MSB) or Foreign MSB with FINTRAC. This mandate has been in effect since June 1, 2020.

To comply, you’ll need to:

- Register your business with FINTRAC.

- Develop a compliance program that includes appointing a compliance officer, conducting risk assessments, and implementing Know Your Customer (KYC) procedures to verify customer identities.

- Report virtual currency transactions over CAD 10,000 to FINTRAC within 24 hours.

- Retain client identification and transaction records for five years.

Additionally, the Travel Rule, effective June 1, 2021, requires MSBs to pass customer identification details for cross-border virtual currency transactions.

While FINTRAC doesn’t charge a fee for MSB registration, businesses should budget for initial setup costs, which typically range from USD 10,000 to 40,000. Annual compliance costs can vary widely, from USD 20,000 to over 100,000, depending on the size and scope of operations.

Securities and Commodities Regulations

The Canada Revenue Agency (CRA) treats Bitcoin as a commodity for tax purposes. However, if your business operates a crypto asset trading platform serving Canadians, you must register with the appropriate provincial or territorial securities regulator and adhere to the guidelines set by the Canadian Securities Administrators (CSA).

The CSA emphasizes:

"To comply with Canadian securities laws, crypto platforms – which sometimes call themselves 'crypto exchanges' – must be regulated by a Canadian securities regulator."

These rules work alongside AML standards to maintain market integrity. The CSA uses a "substance-over-form" approach to decide whether a crypto asset is classified as a security. Security tokens are explicitly covered under securities law, and Initial Coin Offerings (ICOs) may also fall under these regulations if they meet the Investment Contract Test. If your business deals with ICOs, you may need to register as a dealer or file a prospectus, depending on whether your tokens are deemed securities.

Payment Processing Regulations

Bitcoin payment processing falls under FINTRAC's MSB framework. If you’re integrating Bitcoin payment solutions, you must meet both federal and provincial requirements. Registered platforms are expected to secure crypto assets, manage cybersecurity risks, and provide client information during the regulatory review process.

In addition to federal rules, Quebec imposes its own layer of oversight. It is the only province in Canada that regulates MSBs under its Money Services Business Act, which is enforced by the Autorité des marchés financiers (AMF).

Understanding and adhering to these regulations is crucial for businesses that want to operate smoothly while accepting Bitcoin in Canada.

sbb-itb-f81ab9b

Implementing Compliant Bitcoin Payment Operations

Once you've got a handle on the regulatory landscape, the next step is putting systems in place that align with both Canada Revenue Agency (CRA) and FINTRAC requirements - while keeping things running smoothly. The goal? Build a setup that ensures accurate records, minimizes risks, and automates compliance whenever possible.

Recordkeeping for Bitcoin Transactions

The CRA requires detailed records to ensure accurate tax reporting. These records should cover everything you need to calculate the adjusted cost base (ACB), proceeds, income amounts, and whether transactions fall under capital gains or business income. You’ll need to keep these records for at least six years after filing your tax return.

Key details to document include the transaction date and time, CAD value, wallet addresses, exchange used, quantity, and the purpose of the transaction. Even for non-taxable events, proper documentation is crucial to prove ownership and maintain the ACB. This kind of thorough recordkeeping not only meets CRA requirements but also strengthens your ability to manage risks effectively.

Starting in 2026, the CRA will gain access to more detailed data from exchanges under the OECD's Crypto-Asset Reporting Framework (CARF). Crypto Asset Service Providers (CASPs) will be required to report both crypto-to-fiat and crypto-to-crypto transactions, along with customer identification details like name, address, and date of birth. With this increased oversight, your internal records need to be audit-ready and match up with exchange data.

If your business is registered as a Money Services Business (MSB) with FINTRAC, your records also need to support Anti-Money Laundering (AML) compliance. This means documenting large virtual currency transactions of CAD $10,000 or more within a 24-hour period and reporting any suspicious or terrorist-related activity.

Managing Bitcoin Payment Risks

Bitcoin's price swings make risk management a top priority. One effective strategy is converting Bitcoin to fiat immediately, which helps protect against sudden price changes.

Tax classification is another area where missteps can be costly. The CRA determines whether Bitcoin profits are treated as business income (fully taxable) or capital gains (50% taxable) based on factors like transaction frequency, intent to profit, and the commercial nature of your activities. Misclassifying transactions could lead to penalties, so documenting your business model and intent is critical. Generally, Bitcoin received as payment for goods or services is categorized as business income or part of a barter transaction. Using a compliant payment solution can help reduce these risks significantly.

Using Flash for Compliant Bitcoin Payments

Flash takes the heavy lifting out of compliance by automating recordkeeping and risk management. Its advanced tracking and non-custodial wallet-to-wallet solutions are designed to meet Bitcoin payment requirements seamlessly. For example, Flash handles Bitcoin invoicing with USD-equivalent pricing, ensuring transactions are valued at their fair market value in Canadian dollars at the time of each transaction, as required by the CRA.

The platform automatically logs transaction details like dates, times, amounts, and CAD values, making both tax reporting and FINTRAC compliance straightforward. Since Flash operates as a non-custodial solution, you maintain full control over your Bitcoin while the platform takes care of compliance documentation.

Flash also simplifies Bitcoin payments with features like payment links, paywalls, and point-of-sale systems that require minimal technical setup. This allows you to accept Bitcoin without building custom infrastructure, reducing the operational hassle and providing audit-ready records from the start.

Building Governance for Bitcoin Payment Programs

Establishing a robust governance framework is key to keeping your Bitcoin payment operations efficient and compliant with Canadian regulations. This involves setting clear policies, understanding international considerations, and staying on top of regulatory changes that could impact your business.

Defining Bitcoin Payment Policies

Start by creating detailed policies that classify Bitcoin activities. Document factors like transaction frequency, holding periods, market expertise, time investment, financing methods, and advertising efforts. These criteria help determine whether transactions are considered business income or capital gains - an important distinction since misclassification can result in hefty penalties.

Your policies should also address wallet management and transaction approvals. Implement strict controls, such as multi-signature protocols and an approval process, to minimize risks like unauthorized access or errors. If you plan to execute transactions exceeding CAD $10,000 within a 24-hour period, ensure you're registered with FINTRAC and adhere to the anti-money laundering (AML) procedures outlined earlier.

The importance of compliance was underscored in December 2025, when FINTRAC fined Peken Global Ltd. (operating as KuCoin) over $19.5 million for failing to register as a foreign money services business in Canada. During the same period, the CRA's cryptoasset program recovered $100 million in taxes from more than 230 audit files over three years.

In addition to internal controls, businesses must tackle the complexities of cross-border compliance.

International Bitcoin Payment Considerations

If your business accepts Bitcoin from international customers or operates across multiple jurisdictions, domestic compliance measures alone won’t suffice. For offshore crypto holdings exceeding CAD $100,000, you’re required to file Form T1135. Similarly, foreign crypto platforms serving Canadian customers must register appropriately.

Starting in 2027, the Crypto-Asset Reporting Framework (CARF) will introduce annual reporting requirements for cryptoasset service providers. These reports must include details about clients, transaction volumes (both crypto-to-crypto and crypto-to-fiat), and payments or transfers exceeding US$50,000. This global reporting framework builds on the recordkeeping practices discussed earlier, extending them to international operations. If your business operates across borders, collaborate with tax and legal professionals in each jurisdiction to ensure you meet all compliance obligations.

As international requirements continue to evolve, staying informed becomes even more critical.

Tracking Regulatory Changes

Canada is moving toward tighter cryptocurrency regulations, aligning them more closely with traditional financial standards. The Canadian Department of Finance is expected to introduce new legislation by spring 2026 aimed at combating financial crimes, including crypto tax evasion. Finance Minister François-Philippe Champagne emphasized the government’s commitment to addressing these challenges:

"Fraud and financial crime are evolving rapidly, and so must our response. Whether it's launching a new Federal Anti-Fraud Strategy, establishing a dedicated Financial Crimes Agency to combat financial crimes, or addressing economic abuse, our government is committed to safeguarding the financial security of every Canadian."

To stay ahead of these changes, assign someone within your organization to track updates from regulatory bodies like the CRA and FINTRAC. Subscribe to official newsletters, set up alerts for announcements, and schedule quarterly compliance reviews. The CRA has acknowledged challenges in identifying taxpayers in the crypto space, as noted by Olivier Acuna of Coindesk: "There is no way to reliably identify taxpayers operating in the crypto space and assess compliance with income tax reporting obligations". Regular consultations with crypto-savvy tax professionals can help you adjust your policies proactively.

Tools like Flash can simplify governance by automating much of the compliance work. With built-in tracking and reporting features, Flash ensures your records are audit-ready, freeing you up to focus on running your business while staying compliant with changing regulations.

Conclusion: Meeting Compliance Requirements for Bitcoin Payments

Canadian businesses need to understand that the Canada Revenue Agency (CRA) views cryptocurrency as a commodity, not legal tender. This means every Bitcoin transaction is considered a taxable barter event. Depending on the nature of your transactions, income from Bitcoin payments could be classified as business income (fully taxable) or capital gains (50% taxable). Factors like transaction frequency, business intent, and the type of activity determine this classification.

Accurate recordkeeping is critical. Keeping detailed records of each transaction not only ensures proper tax classification but also prepares your business for potential CRA audits. Proper documentation can help you avoid costly penalties and maintain compliance.

To handle Bitcoin payments effectively, businesses should establish a solid governance framework. This includes creating clear policies for Bitcoin transactions, implementing multi-signature controls for added security, and setting up well-defined approval processes. For businesses operating internationally, it’s also important to be aware of and comply with additional reporting requirements.

Staying updated on regulatory changes from the CRA is another crucial step. As regulations evolve, adjusting your processes accordingly will help you remain compliant. Tools like Flash can simplify this by automating compliance tracking and recordkeeping, generating audit-ready reports, and reducing administrative burdens.

FAQs

How does the CRA treating Bitcoin as property impact my tax reporting in Canada?

The Canada Revenue Agency (CRA) treats Bitcoin as property, meaning you must report any profits or losses when you sell, trade, or use it for purchases. Depending on how you're using Bitcoin, these transactions could fall under capital gains (where 50% of the gain is taxable) or be considered business income if your Bitcoin dealings are frequent or part of a commercial venture.

To ensure you're following the rules, it's crucial to maintain detailed records of every transaction. This includes noting the dates, amounts converted to Canadian dollars, and the purpose of each transaction. Keeping organized records not only simplifies reporting but also makes calculating your tax responsibilities much more straightforward.

What records should I keep for Bitcoin transactions in Canada?

To comply with Canadian tax laws, it's crucial to keep comprehensive records of all your Bitcoin transactions. These records should include the transaction date, the amount in Canadian dollars (CAD), the fair market value of Bitcoin at the time of the transaction, and the reason or purpose behind it. Don’t forget to also track acquisition costs, proceeds from sales, and any related expenses, such as transaction fees.

Additionally, make sure to retain proof of wallet ownership and detailed transaction logs. These documents are essential for accurate reporting to the Canada Revenue Agency (CRA) and can help you avoid any penalties for non-compliance.

How can I ensure compliance with anti-money laundering (AML) regulations when accepting Bitcoin payments?

To meet anti-money laundering (AML) requirements when accepting Bitcoin, there are a few important steps to follow. Start by registering your business with FINTRAC as a money services business (MSB). This is a crucial first step to ensure you're operating within the law.

Next, implement processes to verify your customers' identities and keep thorough transaction records. These records are essential for audits and maintaining transparency. Additionally, keep an eye on transactions for any unusual or suspicious activity. If you handle large cash transactions exceeding $10,000 USD within a 24-hour period, make sure to report them to the relevant authorities promptly.

By following these steps, you can integrate Bitcoin payments into your business while staying compliant with AML regulations.