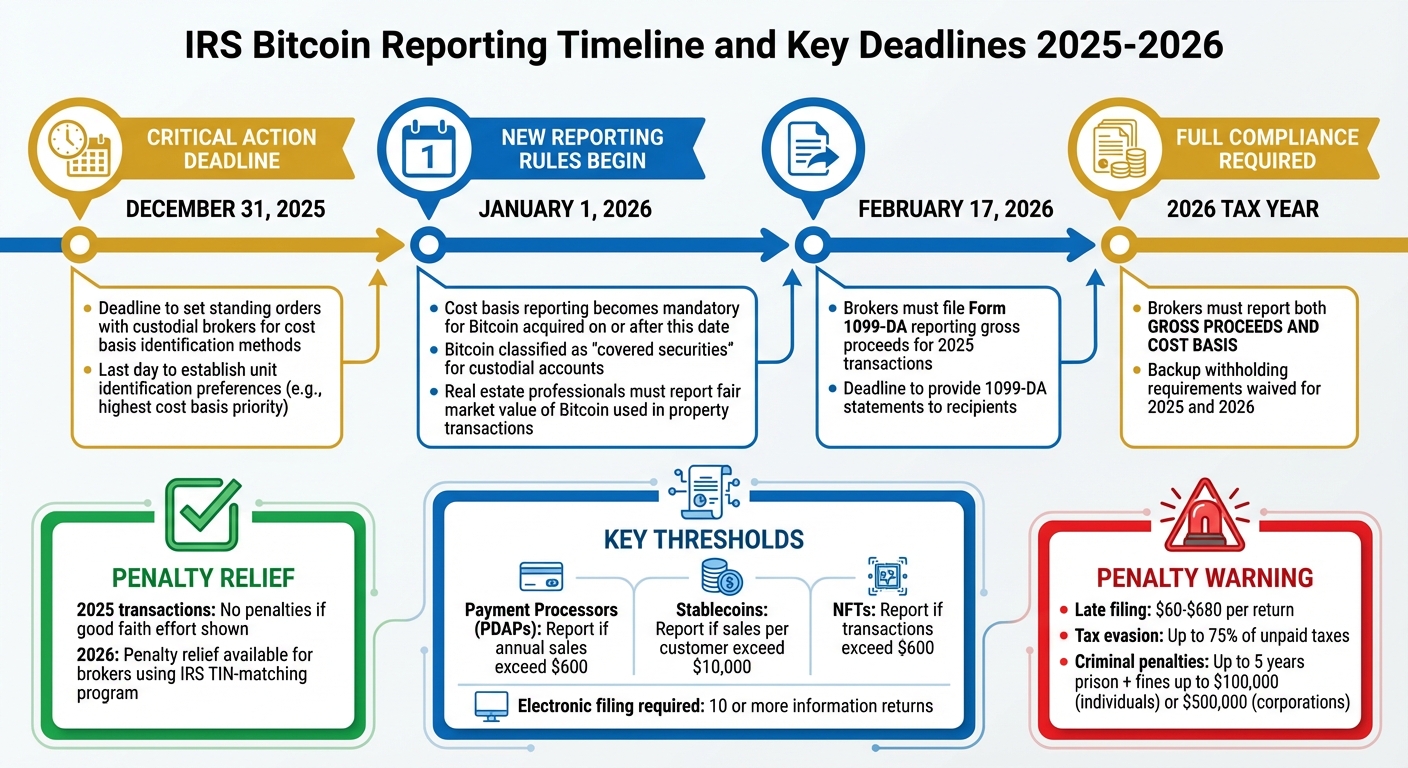

The IRS is introducing new Bitcoin reporting rules starting January 1, 2026. These changes require businesses and brokers to report detailed information about digital asset transactions, including gross proceeds and cost basis for Bitcoin acquired on or after this date. Compliance is critical, as failure to report can lead to penalties.

Key points to know:

- Form 1099-DA: Brokers must report gross proceeds for 2025 transactions by February 17, 2026. Starting in 2026, cost basis reporting becomes mandatory for Bitcoin acquired after January 1, 2026.

- Taxable Events: Selling, exchanging, or using Bitcoin for payments triggers taxable events. Businesses must report Bitcoin payments as ordinary income based on fair market value at the time of receipt.

- Real Estate: Professionals must report the fair market value of Bitcoin used in property transactions starting January 1, 2026.

- Penalties: Late filings can result in fines up to $680 per return, while tax evasion penalties can reach 75% of unpaid taxes.

To comply, maintain detailed transaction records, verify customer information, and use tools like Flash for tracking and reporting. The IRS has provided penalty relief for 2025 transactions if brokers show a good faith effort to comply.

IRS Bitcoin Reporting Timeline and Key Deadlines 2025-2026

Broker Reporting Requirements and Taxable Events

What Brokers Must Report

The IRS has a broad definition of brokers, including custodial trading platforms, digital asset kiosks (like Bitcoin ATMs), and PDAPs that handle Bitcoin transactions. These entities are required to report customer transactions using Form 1099-DA.

For Bitcoin acquired in a custodial account starting January 1, 2026, brokers must report both the gross proceeds and the cost basis (essentially, the original purchase price). These are classified as "covered securities." However, for Bitcoin purchased before that date, brokers are only obligated to report gross proceeds, though they can choose to include cost basis information voluntarily.

Digital asset kiosks must report any transactions where customers sell or exchange Bitcoin for cash or other assets. Additionally, brokers who use the IRS TIN-matching program and successfully match a customer's name with their Taxpayer Identification Number (TIN) can qualify for penalty relief related to backup withholding in 2026.

Bitcoin Transactions That Trigger Taxes

These reporting rules are tied to specific taxable events. Selling Bitcoin, exchanging it, or using it to pay for goods and services all count as taxable events, resulting in either a capital gain or loss. If you receive Bitcoin as payment for services, it must be reported as ordinary income based on its fair market value at the time.

Transaction fees, such as gas fees, can impact your taxable amounts. When selling, these fees reduce your taxable gain. When buying, they increase your cost basis. All fees must be calculated in U.S. dollars.

To minimize taxes, it's crucial to keep detailed records. Use the specific identification method to track which Bitcoin units you sell. If you don’t specify, brokers will automatically apply the First-In, First-Out (FIFO) method, which may not always be the most tax-efficient option. Gains are classified as short-term if you’ve held the Bitcoin for one year or less, and long-term if held for more than a year.

It’s worth noting that certain actions, like transferring Bitcoin between your own wallets or buying Bitcoin with U.S. dollars (which establishes a cost basis), are not taxable events.

How to Comply with Bitcoin Payment Reporting Rules

Using Flash for Reporting and Compliance

To meet IRS requirements, businesses need systems that capture key transaction details, such as timestamps, Bitcoin amounts, and the fair market value (FMV) at the time of the transaction.

Flash simplifies this process with its gateway, which timestamps transactions and instantly converts Bitcoin to USD. This ensures that your internal records align with the data required for IRS Form 1099-DA. Additionally, Flash's invoicing system tracks transaction costs - like gas fees - separately. This feature helps you adjust your cost basis, potentially reducing taxable gains.

Whether you use Flash's payment links, subscriptions, or point-of-sale systems, every transaction generates a detailed record that includes the FMV at the time of receipt. This is essential for correctly reporting Bitcoin received for goods or services as ordinary income. Flash's wallet-to-wallet, non-custodial system automates compliance while ensuring you maintain complete control over your funds.

These automated tools create a strong foundation for accurate recordkeeping, which is discussed next.

Best Practices for Keeping Records

Accurate recordkeeping is crucial for compliance. Keep detailed records of every Bitcoin transaction, including purchase and sale dates, amounts, cost basis, and fees. Consistent documentation works hand-in-hand with automated systems like Flash to meet IRS requirements.

For tax efficiency, consider using specific identification methods. If you hold assets with brokers, you can set a standing order by December 31, 2025, to specify how your units should be identified - for example, prioritizing units with the highest cost basis. It's also wise to separate business and personal wallets. Transfers between your own wallets aren't taxable, but any Bitcoin used to cover transfer fees is considered a taxable event.

Businesses must also answer a mandatory "Yes/No" question about digital asset transactions on federal forms, such as Form 1065 (Partnerships), Form 1120 (Corporations), and Form 1120-S (S Corporations). If you claim a charitable deduction for a Bitcoin donation over $5,000, you'll need a qualified appraisal to back up your claim.

IRS Exemptions and Special Cases

Non-Custodial Transactions and Reporting Thresholds

The IRS has specific exemptions for non-custodial brokers - platforms that don't take possession of digital assets. These brokers are not required to file Form 1099-DA. However, even if you're using non-custodial platforms, like Flash's wallet-to-wallet system, you're still responsible for reporting taxable events on Form 8949. For now, the IRS has deferred Form 1099-DA reporting for activities such as wrapping/unwrapping assets, providing liquidity, staking, lending, short sales, and notional principal contracts.

"The final regulations do not include reporting requirements for brokers commonly known as decentralized or non-custodial brokers that do not take possession of the digital assets being sold or exchanged." – Internal Revenue Service

Payment processors for digital assets (PDAPs) must report transactions only if annual sales exceed $600. For stablecoins, reporting is required on an aggregate basis only if sales per customer exceed $10,000, while NFT transactions have a threshold of $600.

If your digital asset activities are limited to holding Bitcoin in a wallet, transferring it between your own wallets, or purchasing it with U.S. dollars, you can check "No" on the digital asset question on Form 1040. However, using Bitcoin to pay for network fees is still considered a taxable event.

Next, let’s look at how these rules apply to real estate and large transactions.

Real Estate and Large Transaction Rules

When it comes to real estate, special IRS rules apply to transactions involving digital assets. Starting January 1, 2026, real estate professionals - like title companies and attorneys - will need to report the fair market value of digital assets used in property transactions, provided they are aware of such use.

For the 2025 tax year, the IRS is offering penalty relief. Brokers won't face penalties for failing to file Form 1099-DA for 2025 transactions, as long as they can show they made a good faith effort to comply. Additionally, backup withholding requirements for digital asset transactions are waived for both 2025 and 2026.

If you’re donating Bitcoin to a registered 501(c)(3) nonprofit and your claimed deduction exceeds $5,000, you’ll need a qualified appraisal. For deductions over $500,000, a copy of the appraisal must also be attached to your tax return.

sbb-itb-f81ab9b

Penalties for Non-Compliance

IRS Penalties for Reporting Failures

The IRS enforces two main types of penalties: those related to missing information returns (like Form 1099-DA) and those tied to tax evasion or fraud for underreporting income or gains.

For late filing of 2026 information returns, penalties range from $60 per return (if filed up to 30 days late) to $680 per return for cases of intentional disregard.

Tax evasion penalties are far more severe. Civil penalties can amount to up to 75% of the unpaid tax, with maximum fines reaching $100,000 for individuals and $500,000 for corporations. Criminal charges can lead to prison sentences of up to five years. As Michelle Legge, Head of Crypto Tax Education at Koinly, explains:

"The punishments the IRS can levy against crypto tax evaders are steep, as both tax evasion and tax fraud are federal offenses".

Recent cases highlight the consequences of non-compliance. In 2024, Frank Richard Ahlgren III was sentenced to two years in prison and ordered to pay over $1 million in restitution for failing to report $4 million in Bitcoin sales. Similarly, Roger Ver faced charges for mail fraud and tax evasion.

For the 2026 filing season (covering 2025 transactions), the IRS has announced transition relief. According to the agency:

"For transactions occurring in calendar year 2025 (and reported in 2026), the IRS will not impose penalties for failure to file and to furnish Forms 1099-DA if the broker makes a good faith effort to file... correctly and on time".

However, businesses filing 10 or more information returns must submit them electronically to avoid penalties. These strict measures underscore the importance of preparing for compliance well in advance.

How to Reduce Audit Risk

With penalties this steep, reducing the risk of an audit is crucial. The IRS employs data matching and anonymous summons to detect unreported crypto transactions, making audits increasingly likely for businesses that fail to comply. A common trigger for IRS scrutiny is a mismatch between the gross proceeds reported on Form 1099-DA and the amounts declared on tax returns.

To reduce audit risk:

- Keep detailed records, including the fair market value in U.S. dollars, transaction dates, and cost basis for all Bitcoin received as payment.

- Use the IRS TIN-matching program to verify that customer names and identification numbers align with official records.

If you've previously failed to report Bitcoin income, consider filing IRS Form 14457 (Voluntary Disclosure Practice) before the IRS initiates an investigation. Alternatively, you can amend past returns using Form 1040X to pay any owed taxes and potentially avoid harsher fraud penalties. As IRS Commissioner Danny Werfel notes:

"We need to make sure digital assets are not used to hide taxable income, and these final regulations will improve detection of noncompliance in the high-risk space of digital assets".

Answer the digital asset question on your tax return accurately - leaving it blank is not an option and may result in further scrutiny. For businesses using Flash's non-custodial payment gateway, remember that you're still responsible for reporting taxable events on Form 8949, even though Flash doesn’t take possession of your digital assets. Flash's systems can simplify compliance, but businesses must maintain accurate records and procedures to avoid the severe penalties outlined above.

Crypto Catalyst for 2026 + Don't Overpay in Crypto Taxes

Conclusion: Getting Ready for 2026 Bitcoin Reporting

The IRS is making big changes to how Bitcoin transactions are tracked and reported, starting January 1, 2026. Brokers and payment processors will need to report not just gross proceeds but also the adjusted basis for digital asset transactions. Real estate professionals will also have to report the fair market value of any digital assets used in their deals. For the 2025 tax year, the deadline to provide 1099-DA statements to recipients is February 17, 2026.

To stay ahead, consider adopting individual wallet accounting, setting up standing orders with custodial brokers for identifying cost basis, and verifying customer TINs through the IRS TIN Matching tool. This will help you avoid the 24% backup withholding rate.

As one expert put it:

"The IRS is clearly signaling that digital assets are entering a new era of tax compliance. While these changes increase transparency and reporting consistency, they also introduce new risks for investors who are unprepared".

For businesses using Flash's non-custodial payment gateway, accurate record-keeping is essential. This includes tracking the date, time, number of units, and fair market value (in U.S. dollars) for every transaction. Flash's wallet-to-wallet system gives you full control of your Bitcoin while helping you track cost basis and report taxable events, such as on Form 8949. Businesses submitting 10 or more information returns must file electronically using the IRS's IRIS or FIRE systems.

The IRS has also offered some relief: penalty waivers for 2025 transactions, as long as brokers show good faith efforts to comply. Additionally, Revenue Procedure 2024-28 can be used to allocate unused basis for assets held as of January 1, 2025. Keeping independent records will be crucial.

To prepare for 2026, focus on robust tracking systems, early verification of customer information, and maintaining detailed records. With the right tools and processes in place, meeting these new requirements is entirely manageable. By taking these steps now, your business will be ready for the expanded Bitcoin reporting rules.

FAQs

What are the consequences of not following the new IRS Bitcoin reporting rules?

Failing to meet the updated IRS rules for reporting Bitcoin transactions can lead to severe consequences, such as civil penalties or even criminal charges. If you fail to report or underreport digital asset transactions, you could face financial fines, accumulated interest, and, in extreme cases, legal action for intentional non-compliance.

To steer clear of these risks, it's crucial for both businesses and individuals to report all Bitcoin-related transactions accurately and on time, following the IRS's latest guidelines for 2026.

What steps should businesses take to accurately report Bitcoin payments to the IRS?

To properly report Bitcoin payments, businesses need to maintain thorough records of every transaction. This includes receipts, details of sales, exchanges, and any other ways Bitcoin is used or disposed of. For each transaction, it’s crucial to note the fair market value of Bitcoin at the time it was received or spent, along with the date and the purpose of the transaction.

Keeping accurate records not only helps meet IRS requirements but also ensures that businesses stay compliant with tax reporting rules. Additionally, staying updated on the latest IRS guidelines regarding virtual currencies is key to avoiding penalties and ensuring everything is in order.

What types of Bitcoin transactions need to be reported under the new IRS rules?

Under the updated IRS rules set to take effect in 2026, any time you receive digital assets like Bitcoin valued at over $10,000 - whether in a single payment or through related transactions - you are required to report it. This applies to payments for goods, services, or other qualifying transfers.

For businesses, this means keeping detailed records of all Bitcoin payments that meet or exceed this amount. Proper documentation and accurate reporting are crucial to avoid penalties and ensure compliance with tax laws.