Multi-currency wallets are critical for businesses handling Bitcoin and fiat currencies, especially as cross-border payment volumes are projected to hit $250 trillion by 2027. However, integrating these wallets comes with challenges:

- Technical Barriers: Disparate systems use different protocols (e.g., ISO 20022 vs. proprietary APIs), leading to errors and failed integrations.

- Regulatory Hurdles: Compliance with varying KYC, AML, and data protection laws across jurisdictions adds complexity.

- Currency Conversion Issues: Real-time exchange rates, fees, and settlement risks complicate transactions.

- Closed Ecosystems: Many wallets operate in isolation, requiring manual transfers or costly intermediaries.

- Liquidity Constraints: Limited market liquidity for certain currencies can delay transactions or increase costs.

Key Solutions:

- Standardized Protocols: Adopting formats like ISO 20022 improves data consistency and automation.

- Non-Custodial Gateways: Tools like Flash enable direct Bitcoin payments with lower fees and faster processing.

- Hub-and-Spoke Models: Centralized hubs simplify connections and compliance for cross-border payments.

- Local Rails Integration: APIs and local infrastructures streamline regional compliance and enhance connectivity.

By addressing these issues, businesses can reduce costs, improve transaction speed, and better manage multi-currency operations.

Stablecoins, Wallets, and the Rise of Embedded Cross-Border Payments

Common Challenges in Multi-Currency Wallet Interoperability

Interoperable payment systems bring clear benefits, but integrating multi-currency wallets for Bitcoin and traditional currencies presents a range of hurdles. These challenges span technical, regulatory, and operational areas, adding complexity to what should ideally be smooth transactions.

Technical Standards Mismatches

Interoperability depends on aligning technical, semantic, and business layers. Any misalignment disrupts transactions and creates friction.

"Interoperability among payment systems – as the foundation for enhancing cross-border payments – requires technical, semantic and business system compatibility so that end users can seamlessly transact with each other across systems." - BIS Bulletin No 49

A major issue is that wallet providers often use different communication protocols and messaging formats. While some systems have embraced ISO 20022 standards, others rely on proprietary APIs that don't integrate well with external platforms. This leads to data errors and failed integrations between Bitcoin wallets and traditional payment systems. Enterprises must choose from four main interoperability models - single access points, bilateral links, hub-and-spoke setups, and common platforms - each with varying levels of complexity and cost to implement.

But technical barriers are just one piece of the puzzle. Regulatory challenges add another layer of difficulty.

Regulatory and Compliance Complexities

Fragmented regulations are one of the toughest obstacles to adopting multi-currency wallets. Different jurisdictions enforce varying Know Your Customer (KYC), Anti-Money Laundering (AML), and data protection rules, making compliance a constant struggle.

The Travel Rule, which mandates sharing detailed personal data for cross-border payments, adds another layer of friction. Although over 200 jurisdictions have committed to Financial Action Task Force (FATF) standards, inconsistent implementation means enterprises face different compliance requirements depending on the region. By 2030, the introduction of up to 15 retail and 9 wholesale Central Bank Digital Currencies (CBDCs) will further expand the regulatory landscape for multi-currency wallets.

"If designed without a common framework of standards and collaboration, a shortsighted and fragmented approach to CBDC development could lead to the emergence of walled gardens." - Atlantic Council

Bitcoin and other decentralized assets pose additional challenges. Many jurisdictions still grapple with how to regulate unhosted wallets, often resulting in restrictive or conflicting rules. These regulatory complexities also feed into operational difficulties, particularly in currency conversion.

Foreign Exchange and Conversion Challenges

Currency conversion comes with its own set of issues, from accessing real-time exchange rates to dealing with intermediary fees.

"The biggest challenges for currency conversion lie in... Payment tracking, distribution, and settlement/movement of the fiat and digital currency with the FX transaction." - FPC Digital Assets Work Group

Traditional FX transactions often involve asynchronous exchanges, which creates settlement risks that enterprises must manage. For instance, the Continuous Linked Settlement (CLS) system settles transactions multiple times overnight to reduce these risks. Stablecoins introduce another layer of complexity, as maintaining parity between the digital asset and its fiat equivalent requires careful management. Manual processes, inconsistent rules, and jurisdictional limitations further slow down fund availability.

These challenges highlight the need for unified systems capable of handling conversions more efficiently.

Fragmentation of Closed-Loop Wallet Systems

Many wallet ecosystems operate as isolated, closed-loop systems that don't interact with other platforms due to a lack of shared standards and collaboration. This fragmentation forces enterprises to manage separate wallets for Bitcoin, domestic fiat, and international fiat transactions.

Closed-loop systems make seamless value transfer between platforms nearly impossible. Users often have to manually move funds or rely on costly intermediaries. Even when technical connections exist, differing legal and operational rules across jurisdictions can block smooth transactions.

Liquidity and Scalability Limitations

Liquidity is another barrier to seamless wallet interoperability. Robust liquidity management is essential, but many enterprises struggle to maintain it. Limited market liquidity for certain currency pairs - especially when converting between Bitcoin and less-common fiat currencies - can result in poor exchange rates or delays.

Scalability also becomes a pressing issue as transaction volumes grow. Systems need to monitor liquidity across markets or specialized platforms to ensure funds are always available for conversions. While enterprises are exploring more efficient interoperability models like common platforms, the complexity and initial costs of these solutions are often high. The BIS Innovation Hub is currently testing pilot projects to bring these models closer to practical use.

Solutions to Overcome Interoperability Challenges

Tackling the technical and regulatory obstacles previously discussed requires practical strategies that address fragmented systems and reduce reliance on costly workarounds.

Adoption of Standardized Protocols

Adopting ISO 20022 is a critical step toward standardizing financial data across payment systems. Swift began its migration to this standard for cross-border payments in March 2023, with major currencies like the USD, EUR, GBP, SGD, and AUD integrating it into their payment infrastructures. This transition replaces outdated MT messages with structured, data-rich formats, enabling better automation and more efficient transaction screening.

"The ISO 20022 standard can help to overcome barriers linked to the use of these different syntaxes and semantics." - Swift

Financial institutions are encouraged to adopt ISO 20022 reporting messages, such as camt.052, camt.053, and camt.054, as legacy MT category 9 messages are being phased out. This structured approach provides better visibility into cash flows and streamlines transaction monitoring, reducing manual processes.

By building on these protocols, businesses can further improve efficiency through specialized payment solutions like non-custodial gateways.

Using Non-Custodial Gateways Like Flash

Non-custodial payment gateways simplify wallet-to-wallet transactions, offering businesses greater control over their funds. Flash’s Bitcoin payment gateway, for instance, allows companies to accept Bitcoin payments globally while maintaining full control over their private keys. Transactions are processed instantly, bypassing traditional settlement delays.

Merchants benefit from reduced fees by switching to non-custodial models. Flash offers tools like payment links, paywalls, subscriptions, and widgets that integrate with various wallet types - all without requiring businesses to give up custody of their funds. The xPub protocol ensures unique deposit addresses for every order while keeping private keys secure.

"If stablecoins are to define the next era of payments, they need an ecosystem that is permissionless and decentralized." - Siddharth Menon, Founder of PayRam

The non-custodial wallet market, valued at $1.5 billion in 2023, is expected to grow to $3.5 billion by 2031.

Implementing Hub-and-Spoke Interlinking Models

Instead of creating expensive bilateral connections between wallet systems, hub-and-spoke models provide a more efficient alternative. These models offer a single connection point to access multiple domestic real-time payment systems. For example, Project Nexus, developed by the BIS Innovation Hub, connects domestic instant payment systems worldwide, enabling cross-border settlements in under 60 seconds.

Regional initiatives like PAPSS (Pan-African Payment and Settlement System) illustrate how these hubs simplify cross-border payments. Launched in January 2022, PAPSS allows businesses to transact in local currencies without relying on intermediary currencies like the USD. These centralized hubs handle protocol translations and compliance checks, reducing the need for businesses to develop individual integrations for each market.

Adding localized compliance tools can further streamline operations within these models.

Integrating Local Rails and APIs for Compliance

Integrating local payment rails and APIs ensures smoother regulatory compliance and improves system interoperability. Standardized APIs enable real-time data exchange for payment initiation and tracking, simplifying connections between different wallet systems. Collaborating with local banks, mobile wallet providers, and cash agents ensures reliable service delivery while addressing regional regulations.

Programmable APIs can also handle real-time KYC and sanctions checks, while using Legal Entity Identifiers (LEI) for counterparties can help reduce false positives during regulatory screenings. Cloud-native infrastructure capable of processing high transaction volumes across multiple currencies ensures scalability as cross-border payment volumes are projected to reach $290 trillion by 2030.

"For money to move as easily as information, payment networks must speak the same language. That means enabling different systems and currencies to connect seamlessly." - Thunes

These combined solutions create a smoother and more efficient landscape for cross-border payments, helping businesses adapt to an increasingly multi-currency world.

sbb-itb-f81ab9b

Comparison of Interoperability Models

Multi-Currency Wallet Interoperability Models Comparison

Advantages and Disadvantages of Each Model

Selecting the right interoperability model comes down to your business priorities - whether you're focusing on speed, cost efficiency, or meeting regulatory requirements. Each model comes with its own strengths and weaknesses, directly impacting how you handle Bitcoin and multi-currency transactions while addressing the earlier technical and operational challenges.

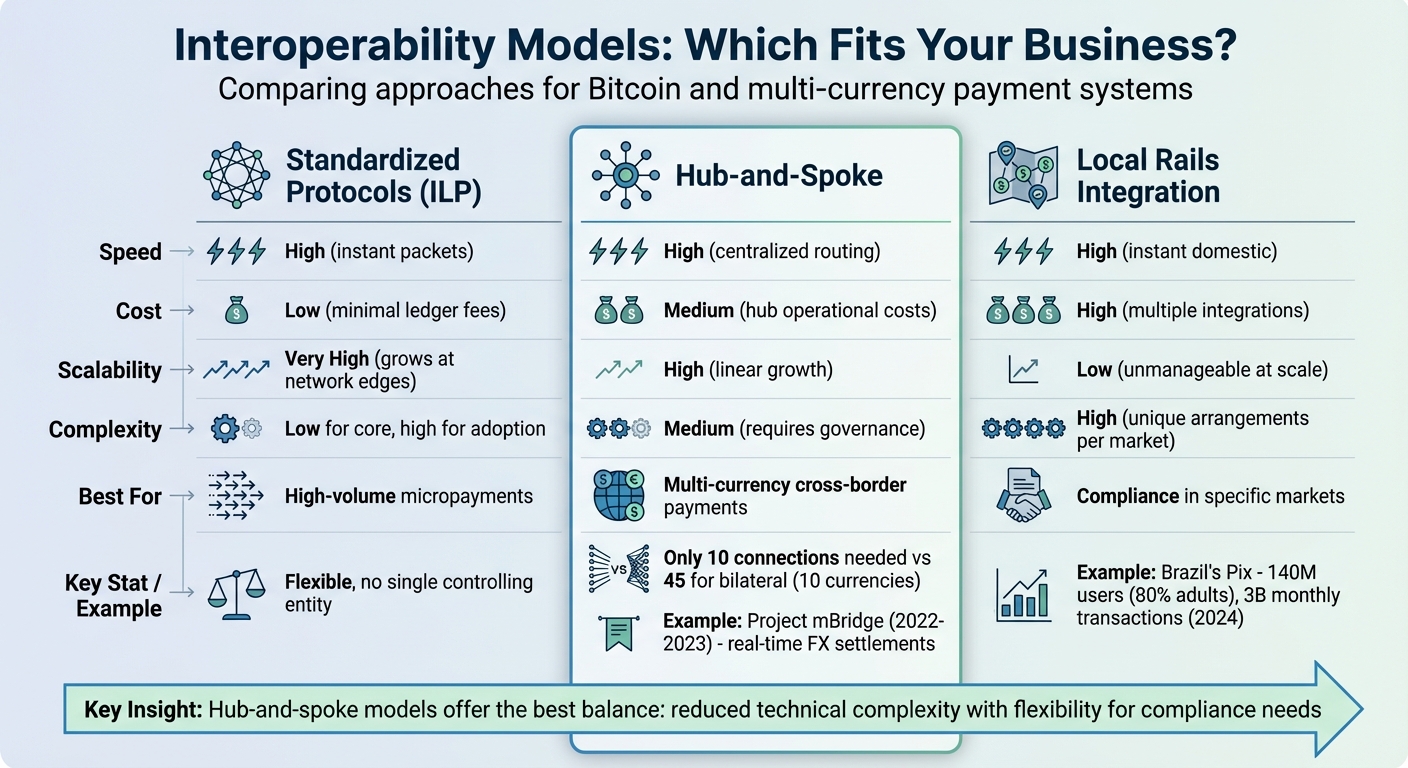

Standardized protocols, such as the Interledger Protocol (ILP), excel in handling high-volume micropayments. Their main advantage lies in their simplicity and independence from any single controlling entity, making them flexible. However, achieving global agreement on standards can be a slow process, particularly in tightly regulated industries.

Hub-and-spoke models simplify connectivity. Instead of needing 45 separate connections for 10 currencies (as required in bilateral setups), you only need 10 connections to a central hub. A great example of this is Project mBridge, launched by the BIS Innovation Hub alongside central banks from China, Hong Kong, Thailand, and the UAE between 2022 and 2023. It showcased real-time peer-to-peer foreign exchange settlements using a shared DLT platform. On the flip side, this model involves centralized governance and higher upfront costs.

Local rails integration delivers the strongest alignment with compliance for specific regions. For instance, Brazil's Pix system reached 140 million users - covering 80% of the adult population - by 2024, processing around 3 billion transactions every month. The downside? Scaling this approach globally is complex, as it requires tailored technical and legal setups for each market.

Here’s a quick comparison of the key interoperability models:

| Model | Speed | Cost | Scalability | Complexity | Enterprise Bitcoin Suitability |

|---|---|---|---|---|---|

| Standardized Protocols (ILP) | High (instant packets) | Low (minimal ledger fees) | Very High (grows at network edges) | Low for core, high for adoption | Best for high-volume micropayments |

| Hub-and-Spoke | High (centralized routing) | Medium (hub operational costs) | High (linear growth) | Medium (requires governance) | Best for multi-currency cross-border payments |

| Local Rails Integration | High (instant domestic) | High (multiple integrations) | Low (unmanageable at scale) | High (unique arrangements per market) | Best for compliance in specific markets |

These comparisons underline the trade-offs enterprises face. Hub-and-spoke models often strike the best balance, reducing technical complexity while offering flexibility to meet compliance needs at each spoke. Non-custodial gateways like Flash can complement these models, enabling businesses to accept Bitcoin globally while the hub handles protocol translations and regulatory compliance across various systems. By matching the right model to their unique challenges, companies can improve both their Bitcoin and multi-currency payment operations.

Conclusion and Key Takeaways

Multi-currency wallet interoperability isn't just a technical hurdle - it's an economic necessity. With cross-border payment volumes expected to surpass $290 trillion by 2030 and nearly 4 billion digital wallet users projected worldwide, businesses must adapt their systems to stay competitive.

To tackle these challenges, a focused strategy is essential. This includes adopting standardized protocols like ISO 20022, utilizing hub-and-spoke models to simplify connections, and leveraging non-custodial gateways to bypass traditional banking hurdles. As Ruben Salazar from TerraPay aptly states:

"Interoperability fundamentally shifts how the world of global payments operates. It is no longer an option but a necessity for the payments industry".

The growing importance of multi-currency interoperability has spurred the development of practical solutions. Flash, for instance, offers a way for businesses to facilitate direct, wallet-to-wallet Bitcoin payments without intermediaries and with minimal fees. This approach not only reduces compliance burdens but also eliminates inefficiencies inherent in traditional systems. Its non-custodial model ensures businesses retain full control while providing customers with instant, borderless payment options.

Modernizing transaction infrastructure is a crucial step toward achieving true interoperability. Key actions include validating transactions server-side, securing API credentials with environment variables, and deploying real-time webhooks. These measures enhance both security and scalability, equipping businesses to handle the complexities of multi-currency operations effectively.

With average cross-border payment costs at 6.3% and remittance flows exceeding $800 billion annually, improving interoperability is a direct route to boosting profitability. By addressing these challenges now, businesses can position themselves for a future where seamless, instant, and integrated multi-currency transactions become the norm.

FAQs

What are the biggest technical obstacles to making multi-currency wallets work together seamlessly?

Achieving smooth interoperability between multi-currency wallets is no easy task. The main issue lies in the variety of technical standards, protocols, and system architectures that different platforms use. These differences can make it tough for wallets to communicate effectively, especially when dealing with cross-border transactions.

Another significant challenge is the lack of alignment on shared standards for real-time, multi-currency transactions. This involves standardizing elements like data formats, transaction protocols, and currency conversion methods - whether for traditional fiat currencies or digital assets like cryptocurrencies. On top of that, wallets must navigate diverse security and regulatory requirements across different regions, which adds even more complexity.

To address these issues, creating interoperability frameworks, cross-chain protocols, and standardized APIs is crucial. These tools can act as bridges between systems, enabling secure, efficient, and instant asset exchanges across platforms.

How do different regulations affect multi-currency wallet integration?

Integrating multi-currency wallets is no simple task, largely due to varying regulations across regions. In the United States, businesses face a dual layer of compliance: federal laws like the Bank Secrecy Act and state-specific rules such as New York’s BitLicense. These regulations not only increase compliance costs but also add operational hurdles that can slow down implementation.

In the European Union, businesses must meet strict anti-money laundering (AML) and know-your-customer (KYC) standards. On top of that, obtaining licenses like the Crypto-Asset Service Provider (CASP) license adds another layer of complexity to operating within the region.

Globally, the situation becomes even more intricate. In areas such as Asia-Pacific, fragmented regulatory frameworks make cross-border transactions and wallet interoperability a significant challenge. While efforts are underway to streamline and modernize these rules, businesses still face a steep climb in creating a smooth, unified experience for managing multi-currency wallets.

What advantages do non-custodial gateways offer for Bitcoin payments?

Non-custodial gateways put you in full control of your private keys, meaning you retain complete ownership of your funds without depending on third parties. This setup boosts security and lowers the chances of your funds being frozen or delayed.

These gateways also support quicker transactions and provide better privacy, staying true to Bitcoin’s core values of decentralization and financial freedom. By cutting out intermediaries, non-custodial solutions simplify payments and reduce fees, making them a smart choice for businesses that want secure, efficient, and direct wallet-to-wallet transactions.