Businesses can now account for Bitcoin more accurately. The Financial Accounting Standards Board (FASB) introduced new rules in December 2023, requiring companies to measure eligible crypto assets like Bitcoin at fair value. This change eliminates the outdated impairment model, where losses were recorded, but gains were ignored unless the asset was sold. Now, unrealized gains and losses are reflected in net income, offering a clear and real-time view of Bitcoin's value.

Key Takeaways:

- Fair Value Accounting: Bitcoin is measured at market value each reporting period, showing both gains and losses.

- Simplified Reporting: No more irreversible write-downs; Bitcoin payments are recorded at fair value upon receipt.

- Eligibility Criteria: Applies to specific crypto assets like Bitcoin, excluding NFTs, stablecoins, and company-issued tokens.

- Effective Date: Rules take effect January 1, 2025, with early adoption allowed.

These updates make Bitcoin payments easier to manage, improve transparency, and align financial reporting with market realities.

New Crypto Assets Accounting and Disclosure Requirements: Understanding and Implementing ASU 2023-08

What the New FASB Crypto Asset Accounting Standards Cover

ASU 2023-08 introduced Subtopic 350-60, laying out clear criteria for determining which crypto assets qualify for fair value measurement. However, not all digital assets are included - this guidance focuses on a specific subset of crypto assets that meet six defined requirements.

Which Crypto Assets Are Covered

Under these new rules, Bitcoin qualifies because it meets all six criteria established by FASB. For a crypto asset to be eligible, it must:

- Be an intangible asset without physical substance

- Lack enforceable rights to goods or services

- Exist on a blockchain or distributed ledger

- Be secured through encryption

- Be fungible

- Not be created or issued by the reporting entity

Assets like NFTs, stablecoins, wrapped tokens, and crypto assets issued by the company itself do not qualify. These remain subject to the traditional intangible asset model. Once eligibility is determined, the next step involves measuring these assets at fair value.

Fair Value Measurement Model

Qualifying crypto assets must be measured at their fair market value at the end of each reporting period. This approach requires companies to recognize unrealized gains and losses in net income, offering a more accurate snapshot of their financial standing.

"I supported our crypto accounting because I felt like whether you're a crypto skeptic or crypto proponent, what we provided was accounting that provided better economics and provided full transparency and I think…we can continue to move in that direction, no matter how people view cryptocurrencies today, with adding this project."

- FASB Board Member Frederick Cannon

In addition to measurement, the new standards specify timelines and transition protocols for implementation.

Effective Dates and Transition Requirements

The new rules take effect for fiscal years beginning after December 15, 2024 - meaning January 1, 2025, for companies operating on a calendar year. Early adoption is permitted, but companies adopting mid-year must apply changes retroactively to the start of the fiscal year. The adoption process follows a modified retrospective approach, requiring a cumulative-effect adjustment to opening retained earnings. Public companies must also disclose the impact in their annual filings under SAB 74.

For companies with substantial crypto holdings, early adoption can improve transparency. Meanwhile, businesses with limited exposure may choose to wait until the mandatory deadline. These updated standards aim to streamline accounting practices and address prior challenges in reporting Bitcoin payments effectively.

How the New Rules Make Bitcoin Payment Adoption Easier

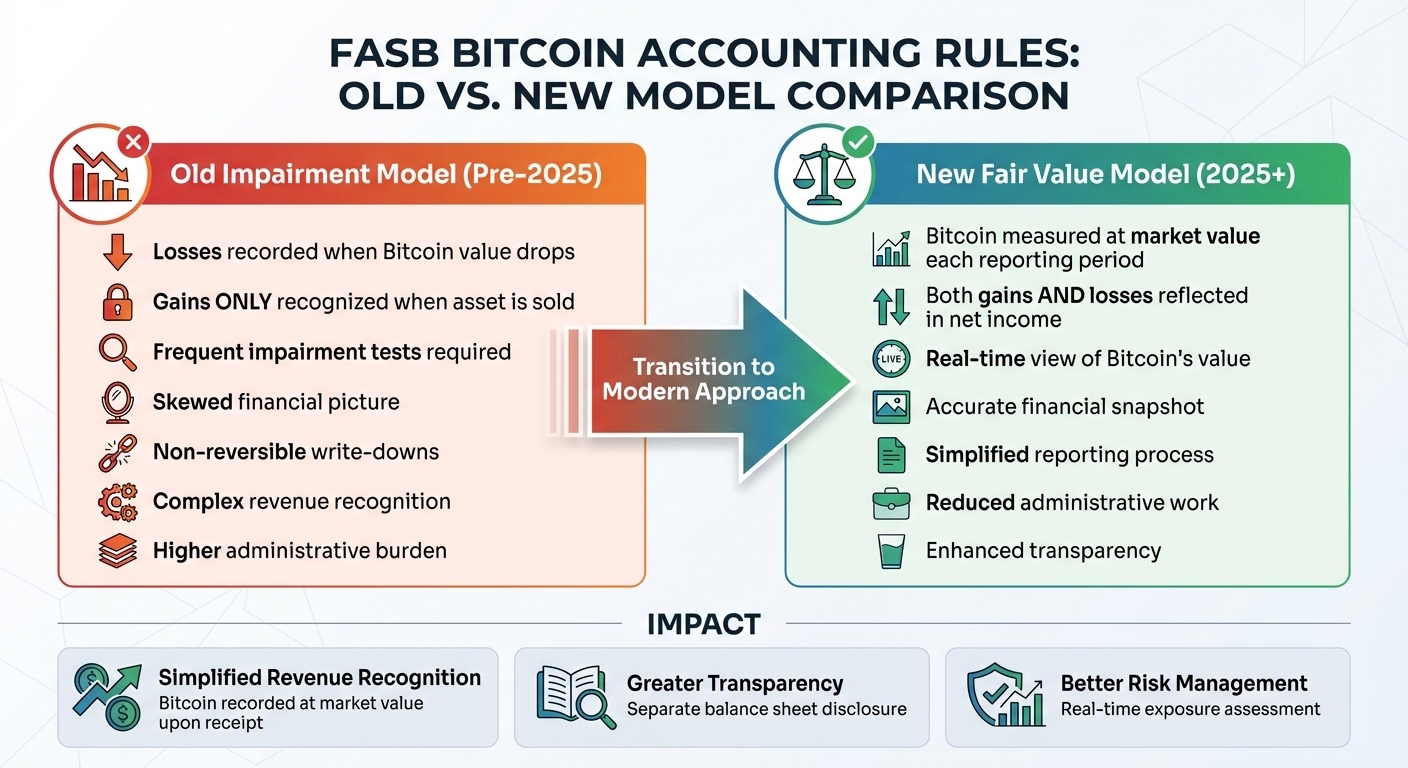

Old vs New FASB Bitcoin Accounting Rules Comparison

The introduction of fair value measurement rules has tackled some of the biggest challenges in Bitcoin payment processing. Previously, the non-reversible impairment model made it difficult for businesses to embrace Bitcoin payments. Under that model, companies could only record losses when Bitcoin's value dropped, while gains were only recognized after selling the asset. This created a skewed financial picture, making Bitcoin payments seem riskier than they actually were for treasury operations.

Simplified Revenue Recognition for Bitcoin Payments

With the new rules, Bitcoin payments are now recorded at their market value upon receipt, and any gains or losses are reflected directly in net income. This aligns with how businesses actually manage Bitcoin - treating it as a liquid asset that changes with market conditions - rather than forcing it into an outdated framework for intangible assets.

The old methods required frequent impairment tests, which complicated revenue recognition and added unnecessary administrative work. The updated standard reduces this burden, making revenue processes more straightforward. This clarity not only helps finance teams but also gives stakeholders a better understanding of financial performance.

Greater Transparency and Investor Confidence

The new rules also improve transparency by requiring companies to disclose how Bitcoin payments affect their financial performance. Crypto assets must now be listed separately on the balance sheet, with gains and losses clearly shown in net income statements. This level of detail addresses concerns about hidden risks and provides the kind of actionable information investors and stakeholders need.

These changes stem from feedback that highlighted crypto accounting as a critical area for improvement. By reflecting Bitcoin’s real-time market value instead of its historical cost, financial statements now offer a more accurate view of a company’s exposure and performance. This added clarity builds trust among investors, auditors, and board members.

Enhanced Treasury and Risk Management

Treasury teams are also better equipped to handle Bitcoin’s volatility under the fair value method. Real-time market value updates on balance sheets give risk managers the tools they need to assess exposure accurately and decide when to convert Bitcoin to fiat currency.

Additionally, classifying crypto transactions as part of operational cash flows simplifies liquidity management and reporting. This alignment with other operational activities makes it easier to integrate Bitcoin payments into existing financial workflows. By reducing operational costs and improving visibility into risks, the new rules support enterprise goals for efficiency and stronger internal controls.

sbb-itb-f81ab9b

How to Account for Bitcoin Payments Under the New Rules

The updated FASB standards under ASU 2023-08, codified as ASC 350-60, provide a clear framework for managing Bitcoin payments in financial statements. The focus is on fair value measurement at each reporting period, with any changes directly impacting net income. Here's how to handle Bitcoin transactions under these guidelines:

Revenue Recognition and Initial Bitcoin Valuation

When your business accepts Bitcoin as payment for goods or services, you must record the revenue in U.S. dollars based on the Bitcoin's fair value at the transaction date. Typically, this involves using the market price from the exchange where your company would convert Bitcoin to cash. This same fair value serves as the initial cost basis for the Bitcoin asset on your balance sheet.

Make sure to present Bitcoin separately on the balance sheet, distinct from other intangible assets. For major cryptocurrencies like Bitcoin, consider listing them as individual line items. This approach provides transparency for investors and stakeholders, ensuring they can clearly understand your exposure to cryptocurrency without it being mixed with assets like patents or trademarks.

After recording the initial value, Bitcoin's fair value must be updated regularly, as outlined below.

Ongoing Measurement and Reporting

Under the fair value model, Bitcoin holdings must be remeasured at current fair value at each reporting period - typically quarterly for public companies. Any gains or losses are immediately reflected in net income. This represents a major change from the previous impairment-only model, which only allowed losses to be recorded until the asset was sold.

Fair value changes related to Bitcoin are shown separately on the income statement, distinct from other intangible asset adjustments like amortization. Whether these gains or losses are classified as operating or nonoperating income depends on your business's circumstances. For instance, if Bitcoin payments are a core part of your operations, they may fall under operating income; otherwise, they could be classified as nonoperating.

Your annual financial reports must include detailed disclosures about your Bitcoin holdings. These should cover the asset name, cost basis, fair value, and the number of units for each major cryptocurrency, ensuring full transparency for stakeholders.

Once remeasured, you’ll need to address Bitcoin-to-dollar conversions as described next.

Accounting for Bitcoin-to-Fiat Conversions

When converting Bitcoin to U.S. dollars, calculate the realized gain or loss as the difference between the sale price and the cost basis. This amount is recorded in net income. It’s important to establish a consistent cost basis method - such as FIFO (first-in, first-out), specific identification, or average cost - and disclose this method in your annual financial statements.

For cash flow purposes, conversions of Bitcoin received as payment in the ordinary course of business - when processed within hours or a few days - are classified as operating cash flows. This simplifies your cash flow statement by aligning Bitcoin payment processing with other operational activities, making it easier to assess your company’s liquidity. Keep detailed records of Bitcoin acquisitions to ensure accurate calculation of realized gains or losses during conversions.

Using Flash to Accept Bitcoin Payments Under the New FASB Rules

With the new FASB rules simplifying revenue recognition and improving transparency, Flash offers a tailored solution for businesses looking to accept Bitcoin payments. It facilitates secure, wallet-to-wallet transfers, ensuring every transaction is clearly documented.

How Flash's Features Support Financial Reporting

Flash simplifies financial reporting with features designed for precision and ease. Its invoicing tool automatically records essential details like timestamps, while real-time analytics allow businesses to review Bitcoin inflows promptly. Customizable payment links and product pages make reconciliation more efficient, and Lightning Network support ensures transactions settle quickly, even during volatile market conditions. Together, these features help businesses maintain smooth and efficient reporting processes.

Simplifying Enterprise Workflows with Flash

Flash integrates seamlessly into existing accounting systems without the need for complex coding. Whether through payment widgets, point-of-sale systems, or custom integrations, Flash connects Bitcoin payment processing directly to your operational workflows. A real-time analytics dashboard further enhances efficiency by tracking Bitcoin-to-fiat conversions, keeping everything organized and accessible.

Maintaining Internal Controls and Security

In line with FASB's focus on transparency, Flash's direct payment model strengthens internal controls. Its non-custodial architecture ensures Bitcoin payments are transferred directly to your enterprise, creating a clear and auditable transaction history. Since Flash doesn’t hold customer funds, your business retains full control over Bitcoin assets from the moment they’re received. This direct approach not only enhances security but also supports your internal verification processes, ensuring transparency at every step.

Conclusion

The updated FASB rules bring clarity to Bitcoin accounting by requiring fair value measurement and removing the need for irreversible impairment testing. This approach aligns financial reporting with Bitcoin's market volatility, allowing companies to present the asset's true economic value on their financial statements. Any changes in value are reflected directly in net income, offering a more accurate picture of Bitcoin's fluctuating nature.

In addition to improving financial reporting, the rules strengthen internal controls and risk management. Enhanced disclosures and valuation practices help minimize fraud risks and boost investor confidence. Businesses that handle Bitcoin responsibly under these guidelines can foster greater trust, which may attract more investment and potentially lower their cost of capital.

These regulatory changes also pave the way for new solutions. For example, Flash's non-custodial payment system aligns perfectly with the FASB standards. It facilitates direct Bitcoin transfers, provides real-time analytics, automates invoicing, and supports the Lightning Network - ensuring an auditable and up-to-date transaction record.

FAQs

How do the new FASB accounting rules affect businesses with small Bitcoin holdings?

The updated FASB rules streamline how companies account for Bitcoin by requiring it to be reported at fair value. This approach offers greater clarity and ensures that financial statements better reflect real-time gains or losses. For businesses, this adjustment simplifies managing Bitcoin assets and incorporating them into financial reports.

That said, there’s a potential downside to consider. Reporting Bitcoin at fair value could lead to higher tax liabilities on unrealized gains, even if the Bitcoin remains unsold. While companies with smaller Bitcoin holdings might find this impact relatively minor, it’s essential to consult financial professionals to fully grasp how this change could affect your specific circumstances.

What should companies consider when adopting the new FASB accounting standards early?

Adopting the new FASB standards ahead of schedule can improve clarity in financial reporting by aligning it with fair value measurement practices. This approach allows businesses to offer more straightforward information about their digital asset holdings, including cryptocurrencies like Bitcoin.

That said, early adoption isn't without its hurdles. It could lead to fluctuations in earnings, create tax-related concerns, and bring complexities in implementation. Companies should weigh these factors carefully and ensure their teams are equipped to handle the transition smoothly.

How does fair value accounting improve transparency for Bitcoin in financial reporting?

Fair value accounting enhances clarity by reporting Bitcoin at its current market value instead of its original purchase price. This method provides stakeholders with an accurate and timely understanding of a company's digital asset holdings and their true financial significance.

By capturing real-time market conditions, fair value measurement minimizes uncertainty in financial statements. This transparency helps decision-makers evaluate performance and address risks more effectively - an essential advantage for businesses dealing with the challenges of digital assets like Bitcoin.