Bitcoin payment compliance in 2026 is more complex than ever. Businesses must navigate new federal laws, international regulations, and stricter enforcement measures. Key updates include:

- GENIUS Act (2025): Establishes rules for stablecoins, impacting Bitcoin payment processors. Businesses must ensure compliance with reserve requirements, audits, and sanctions screening.

- SEC Spot Bitcoin ETPs: Approved in 2024, these provide regulated pricing and custody solutions for Bitcoin payments.

- Travel Rule Updates: Stricter guidelines require detailed sender and receiver information for all Bitcoin transfers, including non-custodial wallets.

- Tax Reporting: Starting January 2026, brokers must report cost basis for Bitcoin transactions, requiring meticulous record-keeping.

Internationally, the EU’s MiCA framework and the UK’s evolving rules demand businesses secure proper licenses and update payment systems. Singapore and Brazil also enforce strict Virtual Asset Service Provider (VASP) requirements.

To stay compliant, businesses should adopt secure payment systems, integrate KYC/AML measures, and track transaction data accurately. Non-custodial payments and Lightning Network integration can simplify compliance while reducing risks.

Understanding these regulations is critical for avoiding penalties and ensuring smooth Bitcoin payment operations.

Managing Crypto Threats in 2026 | Compliance, Fraud & Investigation Strategies

US Regulatory Requirements for Bitcoin Payments

In 2025, the federal regulatory scene shifted with the introduction of the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act), signed into law on July 18, 2025. While the Act primarily focuses on payment stablecoins rather than Bitcoin, it has a notable impact on Bitcoin payment processes, especially when stablecoins are used for settlements. The law officially takes effect in December 2026.

GENIUS Act and Payment Stablecoins

The GENIUS Act establishes a clear framework for payment stablecoins, which are digital assets pegged 1:1 to the U.S. dollar and backed by highly liquid reserves. Only Permitted Payment Stablecoin Issuers (PPSIs) - such as FDIC-insured bank subsidiaries, OCC-licensed nonbanks, and qualified state-licensed entities - are authorized to operate under the Act. These issuers must adhere to strict reserve requirements and provide monthly public attestations, along with annual audits conducted by registered public accounting firms.

For businesses accepting Bitcoin payments, this means ensuring that any payment processor utilizing stablecoins for liquidity or settlements is working with a PPSI. Additionally, state-qualified issuers with over $10 billion in outstanding stablecoin issuance must transition to federal oversight within a year.

The Act also includes several consumer protection measures. Issuers are prohibited from offering interest or yield on stablecoin holdings and cannot market tokens as "government-backed" or "FDIC-insured." Payment systems must be equipped to block or freeze transactions that violate federal sanctions or legal orders. Furthermore, any fees for purchasing or redeeming stablecoins must be disclosed clearly, with a minimum seven-day notice before changes are implemented.

"The Genius Act marks a major milestone in securing America's leadership in payments innovation while protecting consumers and strengthening our national security." – Tim Scott, U.S. Senator

To encourage non-custodial Bitcoin payments, the Act exempts peer-to-peer transfers and hardware or software wallets from intermediary regulations. These updates align with institutional developments like the SEC's approval of Spot Bitcoin ETPs.

SEC Spot Bitcoin ETP Approvals

In 2024, the SEC approved Spot Bitcoin Exchange-Traded Products (ETPs), a significant step forward for institutional Bitcoin adoption. These ETPs offer businesses regulated pricing benchmarks and institutional-grade custody solutions for Bitcoin received as payment. For companies managing Bitcoin in their treasury or converting Bitcoin payments to fiat, ETPs provide transparent pricing and improved access to liquidity.

This regulatory approval has accelerated institutional involvement in Bitcoin. As David Carlisle, Vice President of Policy and Regulatory Affairs at Elliptic, noted:

"2026 will be the year banks progress decisively into digital assets, bolstering the ecosystem's maturation and setting a course for cryptoassets to become a fundamental part of financial services."

Leading financial institutions like JPMorgan Chase, BNY Mellon, and Citigroup have expanded their presence in the digital asset space. JPMorgan Chase CEO Jamie Dimon announced in January 2026 that the bank plans to integrate stablecoins into its financial services to enable faster and more cost-effective transactions. Similarly, Citigroup's leadership has expressed interest in issuing their own token to meet 24/7 client demands. These developments are paving the way for more reliable infrastructure for businesses accepting Bitcoin payments.

CFPB Rules on Digital Payment Applications

In 2025, regulatory changes eased some compliance burdens for Bitcoin payment processors, but consumer protection rules remain a priority. The Consumer Financial Protection Bureau (CFPB) repealed its attempt to classify "larger participants" in digital payment applications, and a proposed rule to extend the Electronic Fund Transfer Act (Regulation E) to crypto was withdrawn in May 2025.

However, state-level enforcement has tightened. For example, New York's proposed CRYPTO Act could classify unlicensed virtual currency activity involving amounts over $1 million as a Class C felony. States like California are also stepping up enforcement against companies operating without licenses, such as New York's BitLicense. Fenwick legal analysts observed:

"State-level enforcements and new laws... signal that regulators are prepared to aggressively pursue remedies, including criminal charges in some cases."

Businesses must also navigate varying state laws related to “junk fees” and surcharges. When implementing Bitcoin payment systems, it’s essential to ensure that convenience fees or surcharges comply with both state consumer protection laws and CFPB guidelines. Under the GENIUS Act, entities classified as Digital Asset Service Providers (DASPs) - defined as those exchanging, transferring, or custodying digital assets for compensation - are treated as "financial institutions" under the Bank Secrecy Act. This classification requires robust anti-money laundering (AML) programs, customer identification (KYC), and sanctions screening.

| Requirement | Federal Qualified Issuer | State Qualified Issuer |

|---|---|---|

| Primary Regulator | OCC (Comptroller) | State Regulator + SCRC Oversight |

| Reserve Ratio | 1:1 (Highly Liquid Assets) | 1:1 (Substantially Similar to Federal) |

| BSA/AML Compliance | Required | Required |

| Transition Trigger | N/A | >$10B Outstanding Issuance |

| Audit Frequency | Monthly (Reserves) / Annual (Financials) | Monthly (Reserves) / Annual (Financials) |

For businesses, this means upgrading financial controls and reporting systems to manage reserve attestations and third-party audits when stablecoin settlement is involved. Additionally, payment systems must include the ability to block or freeze transactions that violate federal sanctions or state laws. As regulatory oversight becomes more structured and state enforcement intensifies, proactive compliance measures are essential to ensure smooth operations.

International Bitcoin Payment Regulations

As the regulatory landscape in the U.S. evolves with initiatives like the GENIUS Act and SEC approvals, businesses with a global footprint face the challenge of navigating a patchwork of international regulations. Regions like the European Union, United Kingdom, Singapore, and Brazil each have their own distinct frameworks for Bitcoin payments and digital asset services, creating complex compliance demands for companies operating across borders. Below, we’ll explore how these key markets approach regulation.

EU MiCA and Transfer of Funds Regulation

The European Union's Markets in Crypto-Assets (MiCA) framework provides one of the most detailed regulatory structures for digital assets. Under MiCA Article 143, the transitional period allowing entities to operate under existing national laws ends on July 1, 2026. After this date, businesses offering crypto-asset services must secure full MiCA authorization or halt operations entirely.

MiCA introduces specific requirements for crypto-asset service providers, including the use of a standardized JSON schema to maintain order book and transaction records. By May 2026, National Competent Authorities will begin requesting transaction data in this new format, following the November 2025 publication of technical specifications. Moreover, all crypto-asset white papers must be submitted in iXBRL format by December 23, 2025, ensuring they are machine-readable and adhere to technical standards.

The Transfer of Funds Regulation (TFR) complements MiCA by strengthening Travel Rule requirements. Businesses are required to integrate KYC (Know Your Customer) and AML (Anti-Money Laundering) measures directly into their payment systems, while maintaining detailed audit trails for regulatory oversight. The European Securities and Markets Authority (ESMA) has also established a central interim register of authorized CASPs (Crypto-Asset Service Providers) and white papers, which will integrate into its IT systems by mid-2026.

For businesses, MiCA represents a significant shift toward standardization across the EU. Companies must secure MiCA authorization well before the July 2026 deadline to ensure uninterrupted operations. Additionally, updating payment systems to support the required JSON message format for transactions will be crucial to meet regulatory expectations starting in mid-2026.

UK Stablecoin Payment Rules

The United Kingdom is charting its own path with a fast-evolving regulatory framework for cryptoassets and stablecoins. While the UK's approach differs from MiCA, the overarching goal is to provide businesses with clear guidelines to operate confidently in the digital payments space.

UK regulations emphasize integrating Travel Rule compliance, VASP (Virtual Asset Service Provider) standards, and robust KYC/AML measures directly into payment systems. These requirements ensure that businesses accepting Bitcoin maintain comprehensive records for regulatory scrutiny. Additionally, UK banks are increasingly stepping into the digital asset space, offering custody and management services for cryptocurrencies.

For businesses operating in both the UK and the EU, choosing payment partners that support domestic acquiring in each jurisdiction is key. Domestic interchange rates can significantly reduce costs compared to cross-border processing. Furthermore, the UK employs sandbox initiatives, providing financial institutions with a controlled environment to test stablecoin and digital asset technologies while building regulatory confidence.

Singapore and Brazil VASP Licensing Requirements

Outside Europe, markets like Singapore and Brazil are shaping their own distinct licensing requirements for Virtual Asset Service Providers (VASPs), reflecting regional priorities.

In Singapore, cryptocurrency exchanges and custodial wallet providers must operate under the Payment Services Act, overseen by the Monetary Authority of Singapore (MAS). MAS provides clear guidance on areas like risk management, advertising, and stablecoin regulation, balancing innovation with strict protections for retail users.

Similarly, Brazil enforces specific standards for VASP licensing, requiring businesses to implement comprehensive frameworks for AML and Counter-Terrorist Financing (CTF) compliance. Companies accepting Bitcoin payments must ensure their payment processors hold the necessary VASP licenses and have robust compliance programs in place. This includes transaction monitoring, sanctions screening, and detailed reporting to local regulators.

For global enterprises, the primary challenge is managing compliance across multiple jurisdictions without compromising efficiency. Flexible payment systems that adapt to different regulatory requirements are essential. Non-custodial payment solutions can ease the compliance burden by eliminating the need to hold customer funds, but businesses must still prioritize transaction monitoring and thorough reporting in every market they operate.

Core Compliance Requirements for Bitcoin Transactions

As Bitcoin payment regulations continue to evolve, businesses must adopt strict transaction protocols and thorough identity verification processes. Compliance demands consistency across borders, though specific enforcement details may differ depending on the region. For 2026, two key requirements stand out: the Travel Rule and comprehensive KYC (Know Your Customer) and sanctions screening. These measures are crucial whether your operations are based in New York, London, or Singapore.

Implementing the Travel Rule

The Financial Action Task Force (FATF) updated its Recommendation 16 in June 2025, laying out clear guidelines for Bitcoin transfers. Under this rule, ordering institutions are required to gather and share specific details about both the sender and recipient of a transaction. This includes the payer's full name and an additional identifier, such as their date and place of birth, residential address, or a unique identification number. Before processing the payment, this information must be verified using reliable, independent sources.

To comply, ensure that transfer messages either accompany or precede blockchain transactions. Your internal policies should also allow for quick sharing of Travel Rule information with other institutions - typically within three business days of a request. If a customer's submitted transfer details differ from the existing KYC records, those discrepancies must be reviewed, updated, and re-verified before proceeding. Even when Bitcoin is sent to self-hosted (non-custodial) wallets, the same level of information collection and record-keeping applies, following the retention periods mandated by local laws.

| Type of Transfer | Action Required by Ordering Institution |

|---|---|

| Standard Virtual Asset Transfer | Collect and verify payer info; collect payee name; pass info and tracing data to the next business. |

| Transfer to Self-Hosted Wallet | Collect and verify payer info; collect payee name; maintain detailed transaction records. |

| Merchant Payment | Pass the card/identifier number to the next business; verification of specific payer elements may be exempt. |

| Internal Transfer | Collect and verify info if the institution serves as both ordering and beneficiary; no external message required. |

These steps are supported by strong identity verification protocols to ensure compliance.

KYC and Sanctions Screening

Equally critical to Bitcoin transaction compliance is implementing robust KYC and sanctions screening measures. Businesses must collect key KYC data, including directors' names, addresses, social security numbers, and registration numbers, and verify this information against public records.

Automated screening should be conducted against major international sanctions lists, such as those maintained by the U.S. Department of State, the Specially Designated Nationals (SDN) list, and relevant FATF lists. This process must also identify Politically Exposed Persons (PEPs) to help mitigate risks related to bribery and corruption.

A risk-based approach is essential. Assign risk ratings based on factors like a customer’s location (e.g., sanctioned territories), involvement in cash-based businesses, non-residency, or connections to high-corruption areas. If a client exceeds a set risk threshold, Enhanced Due Diligence (EDD) measures should be implemented.

Additionally, FinCEN’s updated guidance from October 2025 emphasizes aligning Suspicious Activity Reporting (SAR) procedures with best practices for cross-border information sharing while maintaining confidentiality during international Bitcoin transfers. To address the administrative burden of repeated KYC checks, centralized KYC registries have become popular. These registries provide continuously updated customer data, minimizing the need for manual verifications and streamlining compliance processes.

sbb-itb-f81ab9b

Risk Management and Operations

As Bitcoin payments navigate an increasingly complex regulatory environment, operational strength has become as crucial as identity safeguards and compliance measures. Beyond verifying identities and adhering to the Travel Rule, businesses must implement reliable systems to ensure secure Bitcoin transactions. Two major priorities for 2026 stand out: improving transaction verification and settlement to mitigate fraud and volatility, and meeting tax reporting obligations that now demand detailed tracking of cost basis for every transaction.

Transaction Verification and Settlement

To combat fraud effectively, Bitcoin compliance now leans on AI-driven tools like behavioral analytics, device fingerprinting, and pattern recognition. Troutman Pepper Locke highlights this shift:

"While many have said, 'faster payments, faster fraud,' artificial intelligence will be used as a tool to help combat fraud in instant payments and beyond".

For businesses, maintaining both liquidity and compliance in 2026 means adopting next-day multi-currency settlement systems to limit exposure to Bitcoin’s notorious price swings. The Federal Reserve is working on a "payment account" prototype, enabling eligible payment-focused institutions to settle directly through Fed systems like FedNow and Fedwire. Proposed rules cap overnight balances at the lesser of $500 million or 10% of total assets, with implementation deadlines set for July 18, 2026.

For stablecoin transactions under the GENIUS Act, companies should collaborate with permitted payment stablecoin issuers, which are subsidiaries of insured depository institutions or entities chartered by the OCC. Automated dashboards that reconcile all transaction channels are indispensable, as they reduce operational risks compared to manual reconciliation methods.

These operational upgrades also lay the groundwork for meeting stricter tax and broker reporting obligations.

Tax Reporting and Broker Requirements

Starting January 1, 2026, brokers and PDAPs (platforms facilitating digital asset trades) must report the cost basis of Bitcoin transactions. This builds on the gross proceeds reporting requirement that took effect on January 1, 2025. Businesses are now required to track the acquisition date and cost of every Bitcoin unit to accurately complete Form 1099-DA (Digital Asset Proceeds from Broker Transactions). These measures aim to ensure transparent financial records and bolster compliance efforts.

IRS Commissioner Danny Werfel underscored the importance of these new reporting rules:

"These regulations are an important part of the larger effort on high-income individual tax compliance. We need to make sure digital assets are not used to hide taxable income, and these final regulations will improve detection of noncompliance in the high-risk space of digital assets".

Before finalizing these rules in 2024, the IRS reviewed over 44,000 public comments.

| Requirement | Effective Date | Details |

|---|---|---|

| Gross Proceeds Reporting | January 1, 2025 | Total sale amounts reported on Form 1099-DA |

| Basis Reporting | January 1, 2026 | Cost basis tracking for digital asset transactions |

| Real Estate FMV Reporting | January 1, 2026 | Fair market value of Bitcoin in property transactions |

| TIN Matching Relief | Calendar 2026 | Penalty relief for brokers using IRS TIN-matching during onboarding |

To qualify for penalty relief in 2026, brokers must collect each customer’s Taxpayer Identification Number (TIN) and verify it through the IRS TIN-matching program. Payment platforms are also required to issue Form 1099-K for users surpassing $20,000 in payments and more than 200 transactions annually. Businesses should maintain detailed records of transaction costs, such as gas fees and commissions, as these can reduce taxable income. Additionally, Revenue Procedure 2024-28 provides guidance for allocating unused cost basis to Bitcoin units still held as of January 1, 2025.

Current regulations do not apply to decentralized or non-custodial brokers that do not take possession of digital assets, though future rules for these entities are anticipated. Temporary exceptions also exist for activities like wrapping/unwrapping, staking, and lending, pending further IRS guidance.

Regulatory Risk Mitigation Methods

As enterprises gear up for the 2026 compliance landscape, practical strategies are essential to reduce regulatory exposure. A well-structured Bitcoin payment system can play a key role in addressing these challenges. Three standout approaches include: non-custodial wallet-to-wallet payments with Flash, Lightning Network integration for near-instant settlements, and real-time analytics for continuous compliance monitoring. These methods not only streamline operations but also strengthen regulatory adherence, tying back to earlier discussions on transaction verification and risk management.

Non-Custodial Wallet-to-Wallet Payments with Flash

Flash serves as a decentralized platform that directly connects Bitcoin wallets, eliminating the need for intermediary processors. In the U.S., holding the private key to a digital asset often equates to ownership, making this model particularly appealing. By enabling users to maintain control of their private keys, businesses can sidestep the complexities of custodial regulations.

Non-custodial setups reduce regulatory exposure by cutting out traditional intermediaries, aligning with the requirements of the Travel Rule and KYC frameworks. This streamlined approach simplifies compliance while enhancing trust.

Olivia Carter, a Marketing and Bitcoin Expert at Flash, highlights the benefits:

"A flawless payment process builds brand credibility. When a transaction is effortless, it reinforces the customer's perception that your entire business is professional, reliable, and trustworthy."

To ensure security, developers must protect API keys and verify webhook signatures to guard against fraud.

Lightning Network and Instant Transactions

Non-custodial payments address custody risks, but integrating the Lightning Network takes things a step further. By enabling rapid transactions with lower fees, the Lightning Network minimizes settlement times and reduces exposure to market volatility. Flash supports integration with Lightning-enabled Bitcoin wallets, making payments faster and more efficient.

Speedy settlements not only enhance the user experience but also shrink the window of time where price fluctuations or external factors could impact a transaction. This dual benefit of efficiency and risk reduction makes the Lightning Network a valuable tool for compliance-focused enterprises.

Real-Time Analytics for Compliance Monitoring

Flash's real-time analytics tools provide continuous compliance oversight. These tools can detect anomalies - like sudden spikes in activity - early, allowing businesses to address potential issues before they escalate. Automated webhooks deliver instant updates on transaction status, providing a more reliable alternative to manual processes.

Olivia Carter underscores the importance of seamless integration:

"Your webhook endpoint isn't just a technical detail; it's the central nervous system of your payment integration. It's the direct line from the payment provider to your application."

Real-time analytics also create a detailed audit trail with precise timestamps and data lineage, essential for demonstrating compliance with AML/CFT regulations or submitting Suspicious Activity Reports (SARs). As compliance demands grow, businesses that adopt non-custodial systems, leverage the Lightning Network, and utilize real-time analytics will be better equipped to navigate an increasingly complex regulatory environment.

Bitcoin Payment Compliance Checklist for 2026

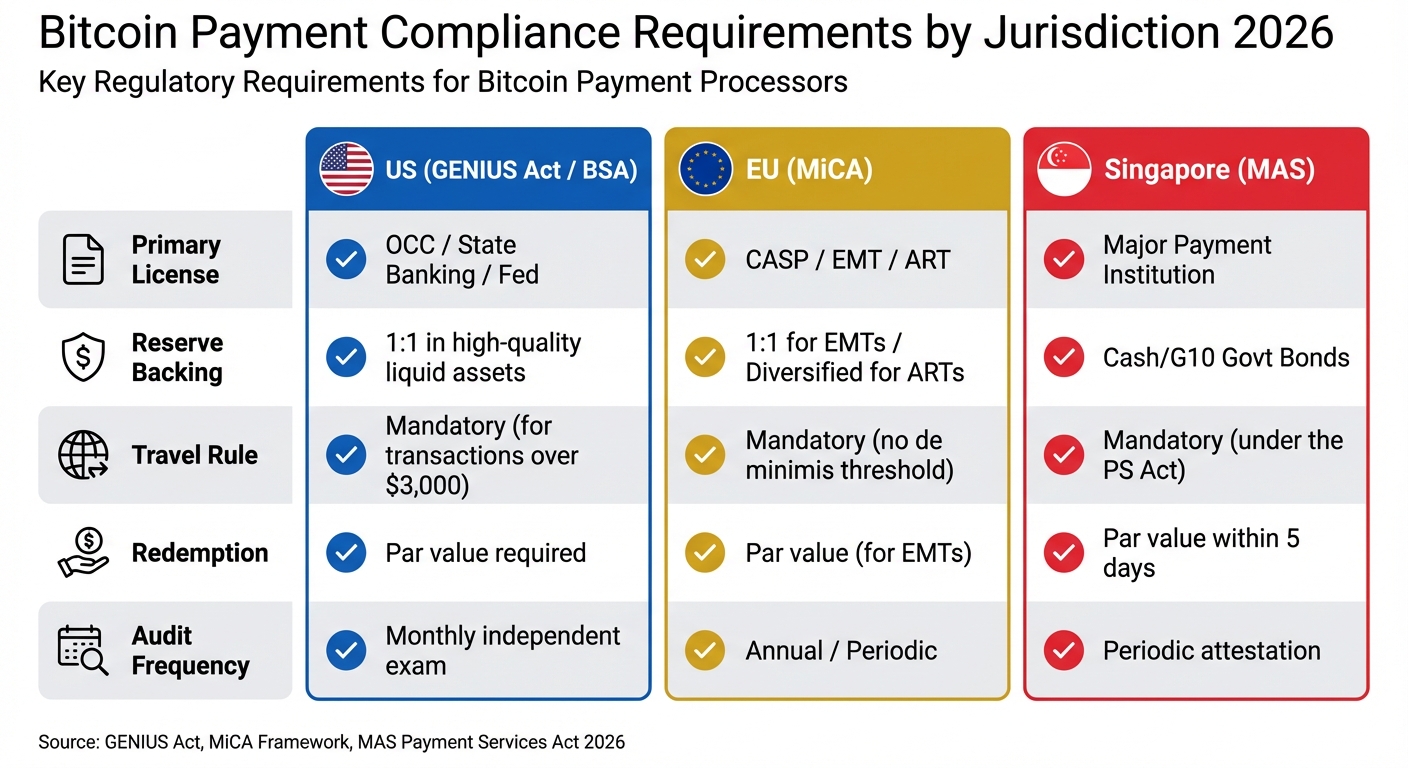

Bitcoin Payment Compliance Requirements by Jurisdiction 2026

Understanding Bitcoin payment compliance in 2026 means knowing how regulations apply to your specific business model and the regions in which you operate. Both U.S. and international regulations now provide clear guidelines for Bitcoin payment compliance. Below, you'll find a summary of the core requirements to help assess your compliance status. These requirements tie directly to strategies and risk management methods previously discussed.

Compliance Requirements by Jurisdiction

Regulatory requirements differ depending on the jurisdiction. In the U.S., a dual framework is in place with federal oversight for stablecoins and state-level enforcement for money transmission. The EU has adopted a unified licensing system for Virtual Asset Service Providers (VASPs), while Singapore enforces strict compliance under its Major Payment Institution framework.

| Requirement | US (GENIUS Act / BSA) | EU (MiCA) | Singapore (MAS) |

|---|---|---|---|

| Primary License | OCC / State Banking / Fed | CASP / EMT / ART | Major Payment Institution |

| Reserve Backing | 1:1 in high-quality liquid assets | 1:1 for EMTs / Diversified for ARTs | Cash/G10 Govt Bonds |

| Travel Rule | Mandatory (for transactions over $3,000) | Mandatory (no de minimis threshold) | Mandatory (under the PS Act) |

| Redemption | Par value required | Par value (for EMTs) | Par value within 5 days |

| Audit Frequency | Monthly independent exam | Annual / Periodic | Periodic attestation |

In the U.S., stablecoin issuers must maintain reserves on a 1:1 basis and undergo monthly audits, as outlined earlier. State-level enforcement continues to play a critical role in ensuring compliance.

Custodial vs. Non-Custodial Systems: Key Differences

The architecture of your system - whether custodial or non-custodial - directly impacts your compliance obligations. Custodial providers, like exchanges and hosted wallets, are classified as Money Services Businesses (MSBs). This classification requires them to register with FinCEN, implement comprehensive AML/KYC programs, and comply with the Travel Rule. On the other hand, non-custodial systems, where users retain control of their private keys, face fewer regulatory demands, functioning more like "publishers of passive code."

Here’s a comparison of the two systems:

| Aspect | Custodial (Exchanges/Wallets) | Non-Custodial (Flash/Lightning) |

|---|---|---|

| Compliance Burden | High (full AML/KYC and Travel Rule) | Lower (focus on code and privacy) |

| Regulatory Oversight | Direct (OCC/SEC/FinCEN) | Indirect (protocol/developer level) |

| Transaction Speed | Moderate | Instant |

| Settlement Risk | Managed by an intermediary | Peer-to-peer / Instant |

| User Privacy | Limited (due to KYC requirements) | Higher (with potential zero-knowledge features) |

| Fee Structure | Higher fees | Minimal fees |

The SEC has clarified its stance on privacy tools, stating:

"Privacy tools should not be presumed illicit and software developers without custodial control should not bear Bank Secrecy Act obligations by default".

This distinction is crucial. If your business operates as a non-custodial platform like Flash, you’re not subject to the same heavy requirements as custodial providers, such as MSB registration, mandatory Travel Rule data sharing, or extensive KYC protocols. However, tax reporting obligations still apply. Starting in the 2026 tax season, custodial brokers will be required to issue Form 1099-DA for digital asset transactions.

Conclusion

As we look ahead to 2026, ensuring compliance with Bitcoin payment regulations is not just a legal necessity - it’s a safeguard against potential crimes, penalties, and operational disruptions. While the reorganization of the Bank Secrecy Act (BSA) regulations may shift administrative details, the core compliance obligations remain firmly in place and legally binding.

For businesses, the stakes couldn’t be higher. Failing to meet compliance requirements can lead to severe criminal and regulatory consequences. These risks highlight the importance of adopting advanced, flexible payment systems to navigate an evolving regulatory environment.

Flash offers a forward-thinking solution by simplifying compliance through direct, non-custodial wallet-to-wallet transactions. By leveraging Lightning-enabled payments, Flash minimizes compliance challenges while delivering instant settlements and ultra-low fees. This streamlined approach not only ensures smooth audits but also supports operational efficiency.

With regulatory focus intensifying - particularly on peer-to-peer payment services - and AI-driven risk assessments becoming more prevalent, businesses that prioritize compliance are better equipped to thrive in both domestic and global markets.

To stay ahead, businesses should regularly monitor updates to FinCEN's 31 CFR Chapter X and conduct thorough audits of third-party providers. Treating compliance as a strategic priority and integrating cutting-edge payment technologies can lay a strong foundation for long-term growth and resilience.

FAQs

What are the key compliance requirements for accepting Bitcoin payments in 2026?

To remain compliant with Bitcoin payment regulations in 2026, businesses in the United States need to prioritize anti-money laundering (AML), know your customer (KYC), and tax reporting protocols. This involves establishing AML programs that include risk assessments, assigning compliance officers, and conducting independent audits. For KYC, verifying customer identities is a must, particularly for high-risk transactions, and businesses are obligated to report suspicious activities involving amounts over $5,000.

Most companies dealing with Bitcoin payments are also required to register as Money Services Businesses (MSBs) with FinCEN and comply with the Bank Secrecy Act (BSA). Keeping accurate records is crucial, as the IRS considers Bitcoin transactions taxable events. Businesses must also account for state-specific rules, like New York’s BitLicense, which adds extra licensing and compliance demands. Staying current with these regulations is key to managing Bitcoin payments legally and effectively.

What impact does the GENIUS Act have on Bitcoin payment processors?

The GENIUS Act establishes a federal regulatory framework for payment stablecoins in the U.S., mandating that issuers adhere to strict standards for licensing, reserves, disclosures, and compliance. This directly impacts Bitcoin payment processors, as they will need to adjust their operations to align with these new stablecoin requirements.

By implementing clear guidelines for how stablecoins are issued and managed, the GENIUS Act seeks to improve transparency and security in digital payments, helping businesses stay within the rules while handling Bitcoin transactions.

What’s the difference between custodial and non-custodial Bitcoin payment systems?

When it comes to Bitcoin payment systems, there are two main types: custodial and non-custodial. Each comes with its own set of advantages and trade-offs.

Custodial systems work by entrusting a third party to manage private keys and hold funds on behalf of the user. This setup is all about convenience - users don't have to worry about managing their own private keys. However, the trade-off is clear: you give up direct control of your funds, relying instead on the third party's security measures.

On the flip side, non-custodial systems put users in the driver's seat. You get complete control over your private keys and Bitcoin, which means greater security and privacy since no intermediaries are involved. But with that freedom comes responsibility - you’re entirely in charge of protecting your private keys. Lose them, and there’s no safety net.