Accepting Bitcoin payments in the U.S.? Here's what you need to know:

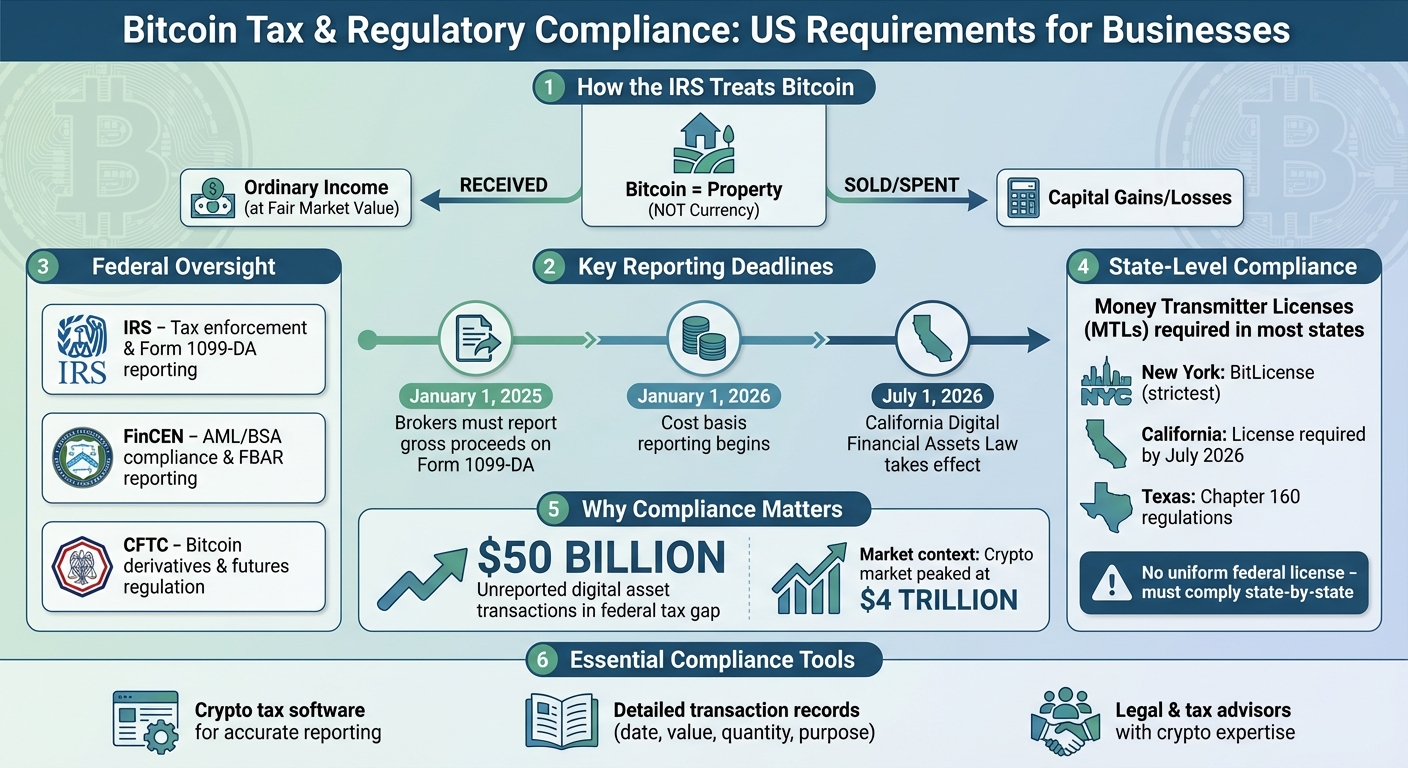

- Tax Classification: The IRS treats Bitcoin as property, not currency. This means every transaction has tax implications - ordinary income when received and capital gains or losses when sold or spent.

- Key Reporting Rules: Starting January 1, 2025, brokers must report gross proceeds from digital asset transactions on Form 1099-DA. Cost basis reporting begins January 1, 2026.

- Federal Regulations: Businesses must comply with IRS tax rules, FinCEN’s anti-money laundering (AML) requirements, and CFTC oversight for derivatives.

- State-Level Compliance: State laws vary widely. Some require Money Transmitter Licenses (MTLs), like New York’s strict BitLicense or California’s upcoming digital asset law in 2026.

- Compliance Tools: Use crypto tax software for accurate reporting, maintain detailed transaction records, and consult legal and tax advisors to navigate complex regulations.

Why this matters: Staying compliant avoids penalties, builds trust, and positions your business as a credible player in the digital asset space. With Bitcoin's growing role in commerce, ensuring adherence to these rules is more critical than ever.

US Bitcoin Tax Compliance Timeline and Key Regulatory Requirements 2025-2026

Demystifying Bitcoin Tax: A Guide to the Current Regulatory Landscape

Tax Implications of Bitcoin Transactions

When dealing with Bitcoin, understanding how it’s treated for tax purposes is just as important as staying compliant with broader regulations.

IRS Classification of Bitcoin as Property

The IRS views Bitcoin as property, not a currency, for tax purposes. This classification means that Bitcoin transactions follow the same tax rules as property transactions. For instance, the fair market value (FMV) of Bitcoin at the time you receive it is considered taxable income. If the value changes before you sell or use it, that change results in either a capital gain or loss when the Bitcoin is disposed of.

Taxable Events Involving Bitcoin

Bitcoin transactions can create two types of taxable events. First, if you receive Bitcoin in exchange for goods or services, it’s treated as ordinary income. You’ll need to report its FMV in U.S. dollars as income at the time of receipt. Second, when you sell, exchange, or spend that Bitcoin, you’ll need to calculate a capital gain or loss based on how its value has changed since you first acquired it. This dual taxation framework highlights the importance of keeping accurate records for each transaction.

Valuing Bitcoin Transactions for Tax Purposes

To ensure proper tax reporting, you must determine Bitcoin’s FMV in U.S. dollars at the time of each transaction. When you receive Bitcoin as payment, its value at that moment becomes your cost basis, which is essential for calculating future capital gains or losses. Additionally, custodial brokers are required to report digital asset transactions under IRS rules, making it even more critical to document real-time valuations. These practices not only help with accurate tax reporting but also align with broader IRS compliance requirements.

Federal Regulatory Requirements

Businesses accepting Bitcoin as payment must navigate a complex web of federal regulations, each overseen by different agencies with distinct responsibilities. These regulations aim to ensure transparency and compliance in the fast-evolving digital asset landscape.

The Internal Revenue Service (IRS) plays a central role in Bitcoin oversight, focusing on tax enforcement. Starting January 1, 2025, custodial brokers will be required to report digital asset transactions using Form 1099-DA, as mandated by new Treasury and IRS regulations. IRS Commissioner Danny Werfel highlighted the significance of these updates, stating:

"These regulations are an important part of the larger effort on high-income individual tax compliance. We need to make sure digital assets are not used to hide taxable income, and these final regulations will improve detection of noncompliance in the high-risk space of digital assets."

The Financial Crimes Enforcement Network (FinCEN) oversees compliance with Anti-Money Laundering (AML) and Bank Secrecy Act (BSA) requirements, ensuring that Bitcoin transactions meet strict financial reporting standards. This includes enforcing Foreign Bank and Financial Accounts (FBAR) reporting rules for virtual currencies. Meanwhile, the Commodity Futures Trading Commission (CFTC) regulates futures contracts and derivatives markets involving Bitcoin, which is especially relevant for businesses engaged in derivatives trading.

Failure to comply with these regulations can result in severe penalties. The IRS has been aggressively targeting crypto tax evasion, recommending hundreds of cases for prosecution. Commissioner Werfel also noted:

"Our research and experience demonstrate that third-party reporting improves compliance."

The Infrastructure Investment and Jobs Act (IIJA) of 2021 further expanded reporting requirements under Internal Revenue Code §6045. This legislation mandates brokers to report digital asset transactions, including sales and exchanges, on Form 1099-DA for transactions occurring on or after January 1, 2025. To meet these federal standards, businesses must keep meticulous records of all Bitcoin transactions, ensuring they are fully prepared for these enhanced reporting obligations.

sbb-itb-f81ab9b

State-Level Regulations

State regulations build on federal standards by adding unique requirements that vary from one jurisdiction to another. Unfortunately, there's no uniform approach to these laws, meaning businesses must navigate a patchwork of rules depending on where they operate.

Money Transmitter Licenses

In most states, cryptocurrency activities fall under existing money transmission laws, which often require businesses to obtain a Money Transmitter License (MTL). Whether your business needs an MTL depends on the nature of your operations - specifically, whether you hold or transmit customer funds or handle monetary value on behalf of others. For example, if your business accepts Bitcoin as payment but doesn’t hold customer funds, you may not need an MTL. However, if you offer payment processing services that involve custody of digital assets, licensing is typically required.

The definition of "money transmission" and "monetary value" varies by state, which can determine whether your cryptocurrency-related activities trigger licensing requirements. New York's BitLicense, issued by the New York State Department of Financial Services (NYDFS), is among the strictest and applies to crypto businesses serving New York residents. Meanwhile, California's Digital Financial Assets Law, set to take effect on July 1, 2026, will require businesses engaging with California residents to secure a license or submit an application by that date unless they qualify for an exemption. Texas also has its own rules under Chapter 160, which impose segregation and reporting obligations on large digital asset service providers and allow for administrative penalties. Understanding these state-specific nuances is essential for businesses before tackling multi-state compliance.

Multi-State Compliance Strategies

For businesses operating across multiple states, it’s critical to evaluate whether their activities - such as holding or transmitting customer funds - trigger varying MTL requirements. Each state has its own set of rules, and companies must comply with the specific regulations in every jurisdiction where they operate. As Carlton Fields explains:

"The specific licenses and registration(s) required depend on a business's activities and the states in which it operates".

Since there isn’t a single federal license for crypto businesses, companies must research and adhere to each state’s money transmitter laws and digital asset regulations individually. To manage this complexity, many businesses turn to compliance specialists who have expertise in navigating state-by-state requirements. Given the constantly changing regulatory environment, professional guidance can help ensure compliance, avoiding costly penalties or disruptions. This highlights the importance of investing in robust compliance tools and expert advice to stay ahead in an evolving landscape.

Tools and Strategies for Compliance

Navigating tax and regulatory requirements can be daunting, but with the right tools and strategies, the process becomes much more manageable. By combining technology, meticulous record-keeping, and expert advice, you can simplify compliance and even turn it into an opportunity for growth.

Using Technology for Compliance

Technology plays a crucial role in streamlining compliance tasks. Advanced tax software with integrated digital asset tracking can help minimize errors and save time. For businesses accepting Bitcoin payments, dedicated crypto payment solutions can automate invoicing, ensure accurate record-keeping, and handle compliance requirements seamlessly. Specialized crypto tax software is particularly useful for generating tax reports. These tools can import transaction data, calculate capital gains and losses automatically, and even provide real-time tax estimates.

For instance, Flash offers real-time analytics to monitor Bitcoin transactions. It operates on a non-custodial wallet-to-wallet model, eliminating the need for additional licensing. Plus, it automates invoicing and payment tracking, creating a clear audit trail. Incorporating such technological solutions into your record-keeping strategy ensures accurate and efficient tax reporting.

Record-Keeping and Reporting Best Practices

Starting in 2025, new IRS rules will require brokers - including custodial digital asset platforms, digital asset payment processors, certain hosted wallets, and real estate brokers handling digital asset transactions - to report transactions on Form 1099-DA. To stay ahead, maintain a detailed ledger that records each transaction's date, U.S. dollar value, quantity, and purpose. This will simplify year-end reporting and ensure compliance with the new requirements.

Additionally, the IRS will mandate wallet-by-wallet accounting beginning January 1, 2025, making accurate cost basis calculations more important than ever. Many businesses find it helpful to keep a separate ledger specifically for Bitcoin transactions, apart from their traditional accounting records. This approach not only organizes information but also streamlines the reporting process.

Working with Legal and Tax Advisors

While technology and solid record-keeping form the foundation of compliance, professional guidance is often the key to navigating complex regulations. Tax advisors with expertise in digital assets can help you understand intricate federal and state requirements while crafting strategies to minimize tax liabilities. If you manage significant or complex crypto holdings, working with a crypto-savvy professional ensures you remain compliant while optimizing your tax position.

For example, Gordon Law Group, a leader in crypto tax services since 2014, has prepared over 1,500 reports using their team of cryptocurrency accountants and tax lawyers. They specialize in troubleshooting crypto tax software issues, particularly for complex transactions involving NFTs, decentralized finance, or niche blockchain activities. This expertise is especially valuable as new IRS reporting requirements, like Form 1099-DA and basis reporting, take effect in 2026.

Professional advisors can also help address past reporting errors before they lead to penalties, audits, or even criminal investigations. Beyond compliance, they can craft tailored tax strategies, such as tax-loss harvesting or leveraging tax-advantaged accounts, to align with your business goals. For companies operating in multiple states, local tax professionals can assist in managing state-specific tax obligations related to cryptocurrency transactions.

Conclusion

Compliance as a Business Advantage

Approaching compliance proactively can turn accepting Bitcoin payments into a major strength for your business. By staying ahead of regulatory requirements, companies build trust with customers, partners, and regulators - an essential edge in a cryptocurrency market that once peaked at nearly $4 trillion.

Effective compliance practices also simplify operations, making tax reporting and accounting more efficient and scalable. Industry leaders understand that strong compliance frameworks not only ensure regulatory alignment but also signal reliability and professionalism to customers. Experts agree that businesses with solid compliance systems enjoy smoother operations and increased customer confidence.

The IRS has ramped up its enforcement efforts, with reports estimating that unreported digital asset transactions account for at least $50 billion of the federal tax revenue gap. By establishing a robust compliance framework now, businesses can avoid costly penalties, audits, and legal troubles. More importantly, this positions your company as a trustworthy and legitimate player in the digital asset space - a quality that attracts customers who prioritize security and transparency. Compliance doesn’t just meet legal requirements; it strengthens your standing in a competitive market.

Next Steps for Enterprises

To capitalize on these compliance benefits, businesses can take specific actions to streamline their Bitcoin payment processes. Keep in mind that new broker reporting rules will require reporting gross proceeds from digital asset transactions starting January 1, 2025, with basis reporting following on January 1, 2026.

- Adopt specialized technology solutions: Platforms designed for digital asset compliance can automate data collection, generate precise tax reports, and maintain clear audit trails. These tools have proven especially effective for businesses handling high transaction volumes.

- Consult crypto-savvy tax and legal experts: Professionals familiar with cryptocurrency's unique tax treatment - ordinary income upon receipt and capital gains or losses upon sale - can help you navigate complex regulations.

FAQs

What are the tax rules for accepting Bitcoin payments in the U.S.?

When you accept Bitcoin as payment in the U.S., the IRS classifies it as property, not currency. This means the Bitcoin's value at the time you receive it is treated as taxable income and must be reported in U.S. dollars. Later on, if you sell or otherwise dispose of the Bitcoin, the difference between its value when you received it and its value at the time of sale is considered a capital gain or loss.

To ensure compliance, it's important to maintain thorough records of all Bitcoin transactions. This includes noting the date, the fair market value in USD at the time you received the Bitcoin, and details of any sales or uses afterward.

What are the state-level regulations businesses need to consider when accepting Bitcoin payments?

State regulations regarding Bitcoin payments can differ significantly, often imposing extra compliance, licensing, or reporting requirements on businesses. These rules can influence how a company operates and may lead to increased costs or added legal responsibilities, depending on the state.

Certain states have established laws addressing digital asset transactions, consumer protections, or licensing for businesses working with cryptocurrencies. Understanding the specific regulations in every state where your business operates is essential to staying compliant and avoiding any legal or financial penalties.

What tools can help businesses meet Bitcoin tax and regulatory compliance requirements?

Businesses looking to streamline compliance with Bitcoin tax and regulatory requirements can turn to specialized crypto tax software. These tools handle tasks like transaction tracking, calculating gains or losses, and generating reports that align with IRS guidelines. Some well-known platforms in this space include CoinLedger, TurboTax, ZenLedger, Koinly, and TaxBit.

Incorporating such software into your financial operations can help minimize errors, save valuable time, and ensure your business stays compliant with U.S. tax laws when handling Bitcoin payments.